Sandwiched in between your accumulation phase and spending phase, the retirement risk zone is often overlooked - to our detriment.

It is the phase of your financial life during which many of the most critical financial decisions will be made - choosing an actual retirement age, choosing when and how to claim social security, conducting a roth conversion strategy, among other things.

This article will seek to explain what the retirement risk zone is, why it is important to think of it as a distinct phase in your retirement planning journey, and specifically - how preparing for sequence of returns risk plays a singularly prominent role during the retirement risk zone period.

Table of Contents

- What is the Retirement Risk Zone?

- What is Sequence of Returns Risk, or Sequence Risk?

- Sequence of Returns Risk and Your Retirement Portfolio

- Timing of Withdrawls

- Effects on Retirement Income

- How to Plan for Sequence of Returns Risk

- Investment Portfolio Allocation

- Bucket Strategy

- Investment Specific Distributions

- Working Longer

- Adjusting Spending

- Dynamic Spending Rules

- Investment Portfolio Allocation

What is the Retirement Risk Zone?

Retirement planning is generally broken into three phases

Phase 1: Accumulation (saving) years - this is the period of time where you try to increase income, decrease expenses, and increase savings rate to create as many investable dollars as possible.

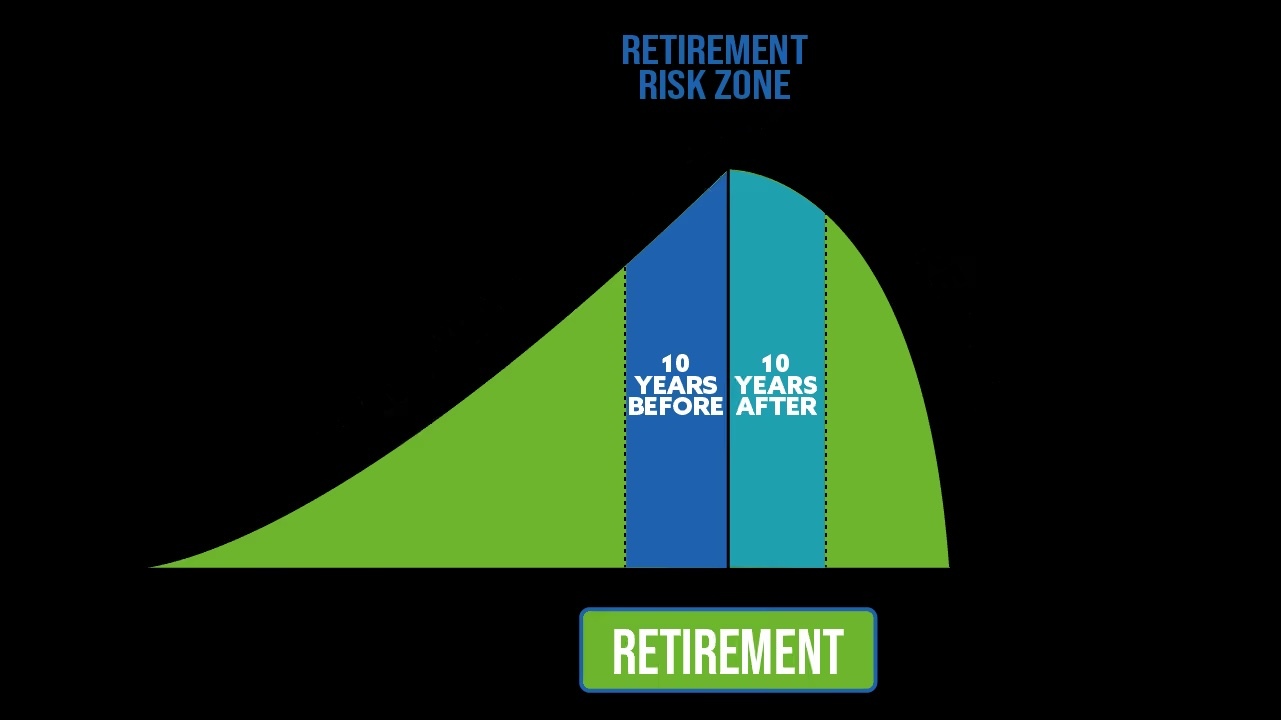

Phase 2: Retirement Risk Zone - this is a transitional phase during which you shift your investment strategy to a more proactive defensive strategy, you identify your required portfolio income, set a target retirement timeline, and learn about things such as social security claiming age, Medicare, IRMAA, etc.

Phase 3: Decumulation(spending) years - this is the period of time where you retrain your brain to spend the money you have accumulated so that you can maintain a high quality of life while not running out of money in retirement..

The Retirement Risk Zone (RRZ) roughly includes the ten-year period prior to retiring as well as the ten-year period after retiring.

It's titled such because during this phase, many of the most consequential decisions of your financial life will need to be evaluated and committed to.

And, as with most financial decisions, there are no do-overs…

Mistakes are permanent… And costly.

Examples of common decisions and actions that are taken during the retirement risk zone include:

- Performing employer sponsored retirement account rollovers into IRA’s

- Possible in-service distributions

- Implementing a ROTH Conversion strategy

- Tax planning to prepare for medicare IRMAA penalties

- Selecting a firm (and prudent) retirement date

- Crafting version 1 of your retirement income strategy

- Selecting your preferred and optimal social security claiming age

- Making retirement portfolio changes

Just as mistakes with all of these actions can be costly - not attending to them at all can be just as expensive in the form of missed opportunities!

It is therefore CRITICAL to understand this phase of life, and navigate it wisely and with good guidance.

The rest of this article will focus on addressing Sequence of Returns Risk as you enter the retirement risk zone.

As you can tell from the list above there are many other considerations to address during the retirement risk zone. For a more thorough exploration of this phase of your financial life, we invite you to watch our FREE webinar titled “Navigating the Retirement Risk Zone”.

In “Navigating the Retirement Risk Zone” we share a planning process that addresses the list of concerns above while also taking into account that you may have individually unique considerations.

You can watch NAVIGATING THE RETIREMENT RISK ZONE HERE.

What is Sequence of Returns Risk, or Sequence Risk?

Sequence of Returns Risk is one of the highest priority risks to defend against as you near or enter retirement.

Thinking strategically about how to play “defense” and protect your retirement assets, you need to ask yourself - what are the behaviors or decisions I have the most INFLUENCE over, and which of those will also have the greatest IMPACT on my retirement portfolio?

At Peak Financial Planning, it is our belief that properly planned for, Sequence of Returns risk can be mitigated, AND better yet, it is actually in your direct control via good decision making.

Sequence of returns risk (SORR) is the risk of negative investment portfolio returns close to or in the early years of your retirement.

Negative retirement portfolio returns are extremely dangerous because they cost you time.

When a portfolio goes down in value by 10%, you don’t need a 10% recovery to breakeven.

You need 11.11% recovery.

When a portfolio goes down by 30%, you don’t need a 30% recovery to breakeven.

You need a 42.86% recovery.

But even more important than the staggering relationship between losses and breakeven recovery is the question of time.

The most important question to be asking here is - “How much time will it take you to recover those unrealized losses, and how does that effect your retirement plan?”.

The chart below shows the exponential relationship as well as the ensuing length of time it would take to recover losses using the historic average rate of return of the SP500.

Unfortunately, as a population we are not informed of this non-linear relationship between losses and recovery periods.

We are told to just “passively invest, set it and forget it, let time do its thing and it will smooth out portfolio losses”.

Unfortunately, this is simply not an acceptable strategy - especially as you enter the retirement risk zone (which we will explain below).

Now, sequence of returns takes the above concept a step further and says - well what happens if you have unrealized losses in your portfolio - but then you ALSO NEED TO TAKE INCOME (DISTRIBUTIONS) from that portfolio in the same year?

Well the combination of unrealized losses with portfolio distributions further exacerbates the problem described above.

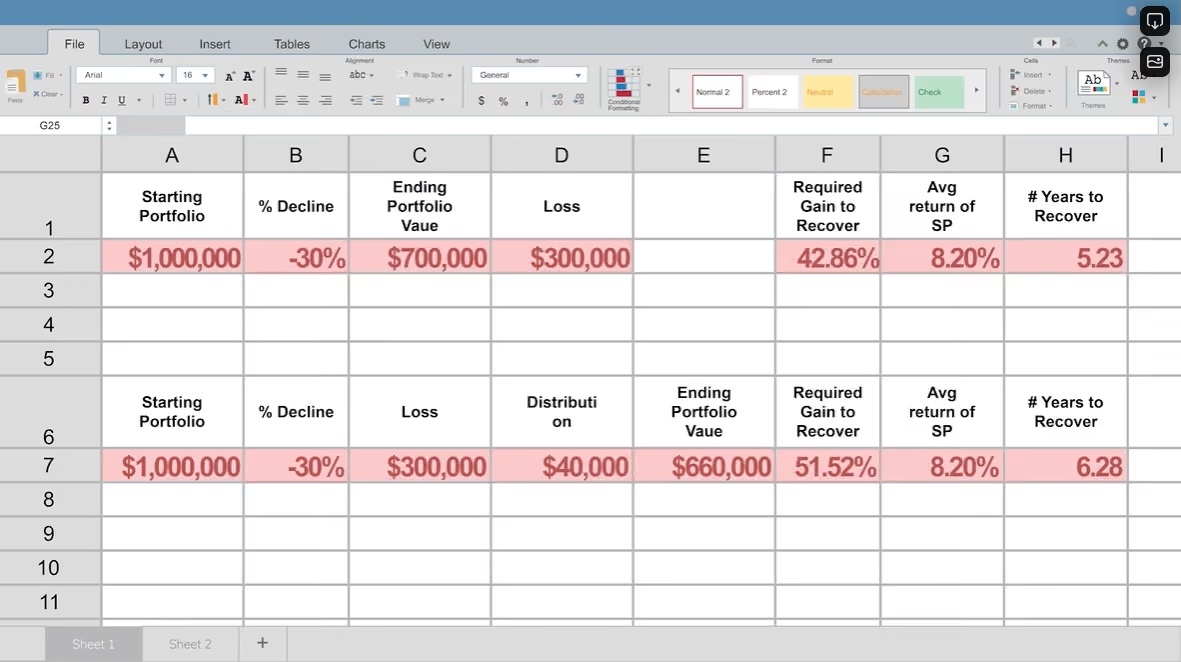

In the image below, you can see that if you were to have a 30% loss in your portfolio, you would need a 42.86% gain to recover back to breakeven.

If you also take a 4% distribution (following the 4% rule - which is another terrible strategy that does not produce good outcomes), you would then need a 51.52% gain to recover back to breakeven.

That 4% distribution requires an additional 9% gain to recover back to breakeven.

More importantly, it increases the number of years to recover from 5.23 years (no distribution) to 6.28 years (with the distribution).

Sequence of Returns Risk and Your Retirement Portfolio

For the purpose of clarity, lets define "retirement" as the point in time when an investor begins to draw income from their retirement portfolio due to a reduction or termination of their primary employment.

The top two reasons to accumulate retirement savings are:

- Support investor living expenses for the duration of their life - meaning investor money must outlive them - not the other way around.

- Support investors with ongoing withdrawals that are predictable and reliable. The investor needs to replace the income lost by leaving their employer.

Let's explore how these objectives are affected when the market declines as investors approach or enter retirement...

Timing of Withdrawals

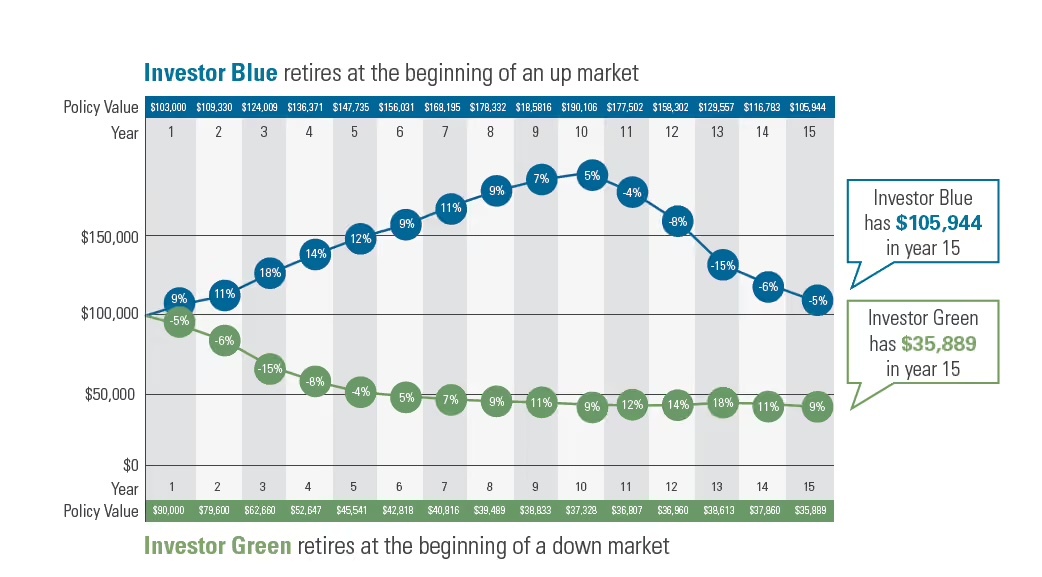

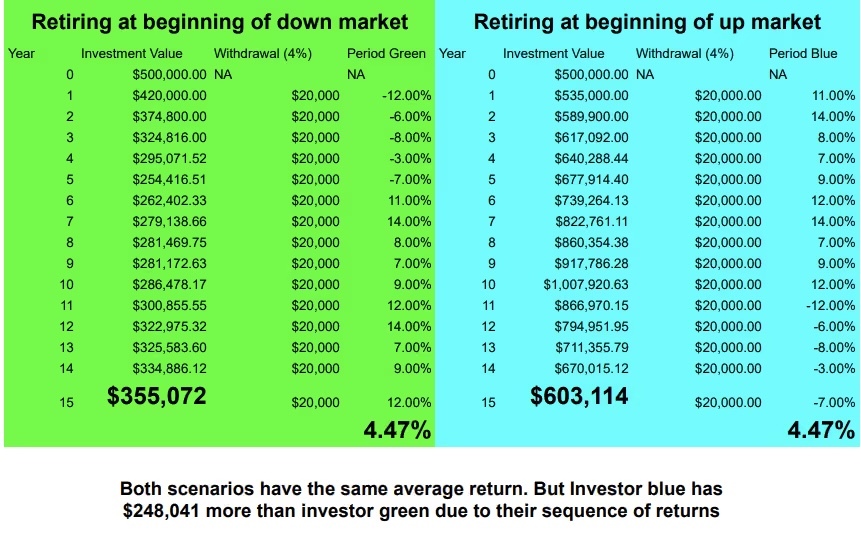

The timing of market downturns REALLY matters when it comes to your ability to take reliable withdrawals from your portfolio.

Investment markets move cyclically - sometimes they go up, sometimes they go down.

Over long time horizons, retirement plans generally assume positive expected returns.

Based on the positive average return expectation, assumptions are then made with regards to the annual withdrawals that can be supported by the portfolio.

When you retire and your starting principal is close to or equal to your target portfolio value - all is well.

But say you have negative investment returns for the 2 years leading up to your retirement and your portfolio is now 20% lower than your target amount.

In this case a certified financial planner will almost always recommend either delaying retiring or spending less money in retirement so as not to deplete your portfolio too quickly.

Effects on Retirement Income

Let's illustrate this with an example:

If you enter retirement with $1,000,000 portfolio value and use a 4% withdrawal rate you would be able to withdraw $40,000.

But lets say the two years leading up to your retirement date are particularly bad years for the markets and your portfolio value upon retiring is only $800,000. A 4% withdrawal rate would result in a $32,000 per year distribution.

The question is - can you get by on less? What if your retirement plan required $40,000 of annual distributions? How will you make up that difference in cash flow?

Not only that - but let's say that 4% withdrawal rate on your $1,000,000 portfolio was calculated to make that portfolio last 30 years of retirement.

If your portfolio value is $800,000 at retirement and you REQUIRE the $40,000 distribution - your portfolio will no longer last 30 years...

Now you risk running out of money early...

The bad sequence of market returns leading up to your retirement date end up being a significant threat to your portfolios ability to support you until end of life...

How to Plan for Sequence of Returns Risk

There are three primary factors that can help manage sequence of return risk.

- How the investors portfolio is constructed while in the retirement risk zone.

- When the investor retires.

- How much the investor spends when retired.

Investment Portfolio Allocation

Investment portfolios are constructed to provide upside potential and outpace the reduction of purchasing power due to inflation.

The higher the risk of the portfolio allocation, the better the portfolio does in achieving its upside and solving for the inflation problem.

However, higher reward also comes with higher risk.

When markets experience a negative sequence of returns, your higher risk portfolio will decrease in value faster than a more conservatively constructed portfolio.

If you are many years out from retirement, your long time horizon will smooth out that risk and allow you to recover.

If you are close to or just entering retirement you will not have that luxury.

For this reason, a more active wealth management approach must be taken when managing an investors investment portfolio while in the retirement risk zone.

Lowering equity allocations as an investor approaches retirement can be one way to solve for this.

But because downturns in the market cannot be predicted, a lower equity allocation can also reduce the potential upside of the investors portfolio.

Investment Specific Distributions

While one is in the retirement risk zone, it is almost always better to perform “investment specific distributions” rather than “pro-rata distributions”.

These days, most investment portfolios are passively managed. The funds in the investment portfolio are likely distributed via an asset allocation into a set of mutual funds, index funds, or exchange traded funds.

When the investor or financial advisor managing this portfolio needs to harvest profits or cash for the portfolio owners distributions, they will typically harvest the funds “Pro-Rata”.

Pro-Rata harvesting is when the portfolio manager sells an equal percentage of all funds within the portfolio in order to come up with the required cash amount for the distribution.

The problem with this strategy is that it does not account for which positions are performing well, and which are performing poorly.

When trying to protect from Sequence of Returns Risk, performing pro-rata distributions is a poor strategy.

A much better one is to perform investment specific distributions - where you harvest cash from funds that have not decreased significantly in value due to poor market performance.

In this way you can harvest "gains from winners” and allow your “losers to lick their wounds”.

An easy example of this would be - if technology stocks are down 15% on the year, but energy or discretionary stocks are only down 2%, you would want to harvest your distribution from the energy/discretionary bucket. This preserves your capital and allows the technology stocks to rebound over time.

Another solution to sequence of returns risk is to use a "bucket strategy".

Bucket Strategy

The bucket strategy divides retirement into distinct time increments that allow investors to choose investments that deliver specified outcomes at specified times.

The bucket strategy can be especially useful during the early years of the retirement risk zone, as it is probably the most effective way to mitigate sequence of returns risk.

Assuming 30 years of retirement, an investor might divide their retirement into three stages:

Stage 1 - the first ten years.

The assets needed for the shorter term bucket are invested into investments that are lower risk and more easily converted to cash. The investments might include laddered bonds, treasury inflation protected securities (TIPS), bond funds, possibly even cash or cash alternatives. This mitigates the risk that a poor sequence of returns seriously depletes that first bucket and leaves the investor without adequate funds to live on.

Stage 2 - the middle ten years.

The assets needed for the second stage are invested into investments that are slightly riskier. It could include some bonds, some equities positioned for growth, maybe even some commodities or real estate. More risk can be taken here because the investor has a longer time frame to ride out market swings.

Stage 3 - the final ten years.

The assets needed for the third and final stage can support the most risk. These investments might include small cap stocks, emerging market stocks, or even high yield bonds. The longer time horizon allows more time for the market to recover before the funds in this bucket are needed.

As the investor moves from stage 1 to stage 2 and eventually stage 3, each buckets' investment allocation is adjusted so that the funds needed on a shorter time frame move to more conservative investments.

Studies have shown that this more active approach to managing a retirees investments can both protect against the downside risk in retirement presented by sequence of returns risk, but also reduce investor anxiety.

Working Longer

Another strategy that mitigates sequence of returns risk is working longer, or delaying retirement.

Working longer shortens an investors retirement period, can increase social security benefits, increase pension benefits (if available), as well as provide additional time for investment growth via savings and market upside.

Studies have found that working an additional 3-6 months longer than planned has the same result as saving an additional 1% of earnings each year for 30 years (EXTREMELY POWERFUL).

Stated another way, working 1 month longer has the same impact as saving 1% of earnings for 10 years.

Adjusting Spending

The third and final strategy that can be used to mitigate sequence of returns risk is to adjust spending using dynamic spending rules.

Dynamic Spending Rules

Most retirement strategies including, the 4% rule, call for annual distributions to be adjusted for inflation.

Using the 4% rule, the retirees initial withdrawal rate would be 4% and then adjust each year for inflation.

Using dynamic spending rules each years withdrawal amount would change to reflect not only inflation but also the markets returns.

When market returns are good and inflation is low, an investor can withdraw more funds from their savings.

When market returns are bad and inflation is higher, an investor would withdraw less funds from their savings.

Dynamic spending rules allow more flexibility but may also require withdrawal decreases or freezes when the markets aren't working in your favor.