Updated: Modern retirement investing strategy is dictated almost entirely by a concept called Asset Allocation.

Asset allocation is the proportional weighting of the money in your retirement portfolio to specific categories of investments, also known as an asset class (asset classes).

Asset classes can be broken into two categories - “Equities”, or stocks, and “Fixed Income”, or bonds.

From there, Equities can be further broken into sub asset classes like growth stocks, value stocks, small cap, large cap, or international.

Fixed Income can be broken down further by the length of the bond, or the issuer of the bond (think 3-month vs 5 year, or US vs. International).

In this article we will explain asset allocation in more depth and make the case that it is a substandard investment framework that leads to poor retirement outcomes.

Short Summary

- Asset allocation is a framework that helps guide retirement investment decisions.

- Asset allocation refers to the proportion of your retirement funds that should be invested in a particular investment category.

- Asset allocation does not provide any detail about individual investments volatility, potential risk, or income produced.

- As such, relying on asset allocation alone to make prudent retirement investment decisions can lead to catastrophic retirement portfolio outcomes.

Table of Contents

- Asset Allocations and the "Buy and Hold Strategy"

- Tactical Asset Allocation vs Strategic Asset Allocation

- What is a Strategic Asset Allocation?

- What is a Tactical Asset Allocation?

- Why We Believe Tactical Asset Allocation is Superior to Strategic Asset Allocation

- What is an Asset Allocation Fund?

- Target Date Fund

- Asset Allocation Fund

- The 3 Fund Portfolio

- How Asset Allocation Strategies Fall Short When Informing Retirement Investing Strategies

- Frequently Asked Questions

Asset Allocations and the "Buy and Hold Strategy"

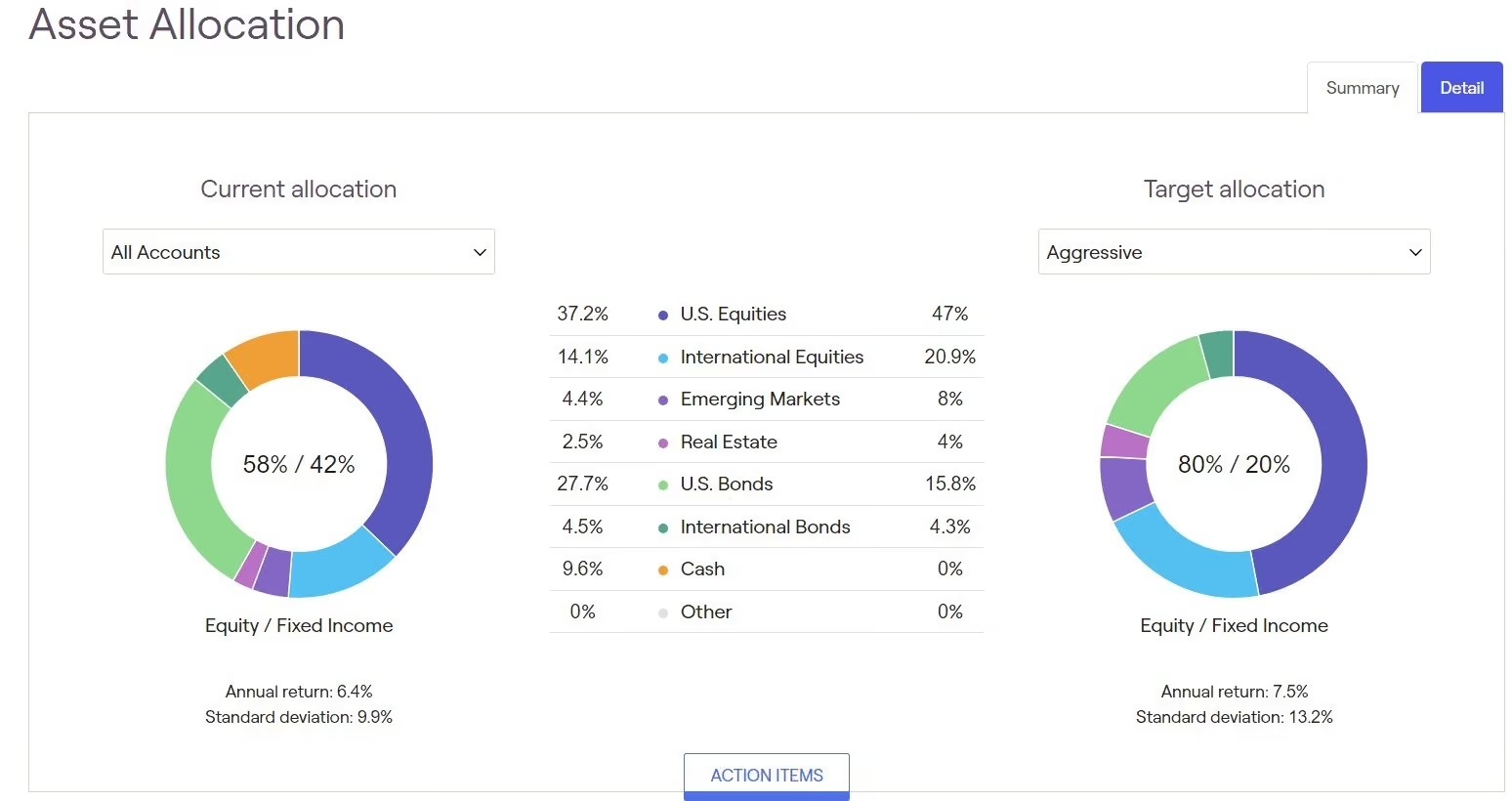

An asset allocation is an investment framework that tells you exactly what percent of your retirement money should be invested in what types of investments.

Asset allocations use historical investment performance data to provide these categorical guidelines.

In the image above, you can see that the example “Aggressive” asset allocation recommends 47% of funds in US Equities, 20.9% in International Equities, 8% in Emerging markets, and so on.

The important thing to note is that it provides CATEGORICAL guidelines without providing any direction into the actual investments that will comprise that 47% of US Equities, or that 20.9% of International Equities.

It is left to you as the investor to then make decisions regarding which individual investments to purchase that will comprise those percentages.

The prevailing wisdom is to combine your investment objectives with an appropriate Asset Allocation (as the broad guideline) and then invest in low-cost Index Funds (Exchange traded funds - ETF’s) or mutual funds when constructing your retirement portfolio.

Index Funds are investments that hold many investments within them.

The idea being that the manager of the Exchange Traded Fund or Mutual Fund has the professional experience to choose the right individual investments, so if you can pick the right ETF or Mutual Fund (pick the right manager) then you don’t need to be the expert on investment selection yourself.

In this scenario, all you need to do is pick funds that match your desired asset class (or asset classes) and thereby do not need to be responsible for the selection of individual companies.

The “Buy and Hold” Investment Approach

The combination of Asset Allocations and low-cost index funds (ETF’s/Mutual Funds) allows for a “buy and hold” investment strategy.

The "buy and hold" approach claims that because historically financial markets have “always” appreciated over time, that if you simply choose the right investment mix based on historical performance (asset allocation) and then hold the investments long enough, they will go up in value.

The idea is to buy and hold and do your best to ignore market conditions, economic events, or negative news - because over long enough periods of time investments ALWAYS go up in value.

Yes - over short periods of time (such as 2008, 2020, 2022) your retirement portfolio may go down in value.

But if you can just ride it out, those losses will recover and be negated by the eventual long-term growth.

At Peak Financial Planning, we wholeheartedly disagree with this concept.

While we do believe there is some merit to the use of asset allocation, we believe there has been a sophisticated propaganda effort aimed at consumers just like you and me.

This propaganda effort is designed to CONVINCE us that a buy and hold, asset allocation strategy is the best method when in fact the ACTUAL investment performance of retiree’s just like you do not support this.

Over the 15ish years that the buy and hold investment strategy has prevailed retirement outcomes have worsened.

The buy and hold strategy has also enabled brokerage companies and financial advisors to become lazy.

No longer are financial advisors actually investment experts. They are now just sales people who’s sole job is to gather investment money without actually being an expert at investing that money!

To illustrate this, we will begin by explaining that there are actually two distinctly different approaches to asset allocation, the Strategic Asset Allocation approach, or the Tactical Asset Allocation approach.

These philosophies use the same foundation of asset allocation as a strategic guideline for your investment money.

But from there they completely disagree with each other on the method of executing and managing the ensuing investment portfolio.

Click here to schedule a free no obligation consultation with our Fee Only Fiduciary Financial Planning team.

Tactical vs Strategic Asset Allocation

Tactical and strategic asset allocation are competing philosophy’s that recommend different levels of involvement in managing one’s retirement portfolio.

Those that believe in the strategic asset allocation philosophy follow a longer term buy and hold investment strategy.

Those that believe in the tactical asset allocation philosophy believe in taking a more active hand in the management of their retirement investments.

What is a Strategic Asset Allocation?

Strategic asset allocation recommends ignoring short/medium investment market performance.

Instead, historical data claims that investment market ALWAYS goes up over long periods of time (periods longer than 10 years).

You would periodically (typically annually) rebalance your retirement portfolio back to the strategic asset allocation risk tolerance as a method of “risk management”.

Rebalancing involves buying or selling investments you already own to bring your portfolio weights (proportions) back to the desired allocation.

For example, the stock portion of your portfolio has risen to 75% of your portfolio value because your top holdings are performing well.

Your goal allocation is a 60% stock/40% bond ratio.

Accordingly, you would take profit (sell) some of your stock holdings and reinvest that profit into bond holdings in order to bring your portfolio back to a 60%/40% ratio.

This more passive approach uses a strategic asset allocation philosophy because you're not selling the stock because you anticipate a shift, you're selling the stock to simply reset your weights in your portfolio's asset allocation.

Therefore, if you have the constitution and discipline to just buy and hold and ride out short term market fluctuations, you will be better off in the long run (because “investments always go up in value”).

For this strategy to bear fruit, you must be able to ride out large market downturns such as the great financial crisis in 2008, Covid in 2020, or the market correction in 2022.

One of the modern attractions of using a strategic allocation strategy is that it is VERY simple.

The process of choosing the appropriate strategic asset allocation involves:

- Use a Risk Tolerance Questionnaire to determine your “Risk Score”

- Your “Risk Score” will determine a ratio of Equity investments vs Fixed Income investments that should be in your retirement portfolio

- Based on that ratio, diversify your investment into low cost index or mutual funds that follow the “rules” of that ratio.

- Rebalance your portfolio annually according to your risk tolerance.

- Sit and watch your retirement portfolio perform.

Because of it’s simplicity, strategic asset allocation is the predominant strategy in the retirement investing universe.

However, just because it is popular does not mean it is actually the best method.

While using a strategic asset allocation can have merit for young, extremely disciplined, low anxiety individuals, it is very hard for the average retirement investor to just watch their portfolio crater in value without making reactive changes to their investment portfolio, thus counteracting the entire strategy…

What is a Tactical Asset Allocation?

Tactical asset allocation is a more hands on investment approach that can preserve capital.

Much the same as with a strategic asset allocation, you begin by constructing an asset allocation (investment guidelines) that is supported by historical data.

Then, over your investing lifetime, you would adjust your portfolio weightings in anticipation of, or in response to, temporary economic circumstances or current market trends.

As market conditions change, you would proactively adjust the investments held in your retirement portfolio.

This is a much more hands on approach that takes a proactive approach to risk management.

The tactical asset allocation philosophy prioritizes taking an active hand in preventing downside risk to your portfolio that includes:

- Using hedges

- Dynamic portfolio weightings

- More frequent rebalancing

- More active profit taking

- More frequent tax loss harvesting.

A tactical asset allocation strategy may recommend increasing the percentage of your portfolio that's in longer duration bonds because of forecasted interest rate cuts or increasing exposure to defensive stocks when expecting economic contraction or recession.

This is different from rebalancing (the primary “risk management” method used in the Strategic Asset Allocation philosophy).

Why We Believe Tactical Asset Allocation is Superior to Strategic Asset Allocation

In the strategic asset allocation philosophy, you are told to essentially just “shut up and take your punches” - that because markets go up over time, losses in your retirement portfolio will be made up if you can just sit and wait it out (this is not exactly true - you can watch this video on our YouTube channel where we show why).

The problem with this approach is that you lose TIME.

The one thing you can never recover is time.

Let me illustrate this with another example (here’s an article we’ve written on this exact subject)

Did you know that in order to recover a 10% loss in your investments value you need an 11.1% gain?

To recover a 20% loss you need a 25% gain.

To recover a 30% loss you need a 42.86% gain.

40% loss requires a 66.67% gain

50% loss requires a 100% gain.

Now the question arises - how long does it take using historic average rates of market returns to actually JUST GET BACK TO BREAKEVEN!

The answer is - for a 10% loss it requires 1.36 years.

For a 20% loss it requires 3.05 years.

For a 30% loss it requires 5.23 years.

For a 40% loss it requires 8.13 years.

For a 50% loss it requires 12.2 years.

When your portfolio returns are negative, you’re not just losing money, you are losing potentially catastrophic amounts of TIME.

Knowing this, we believe that this passive, buy and hold, strategic asset allocation strategy only benefits brokerage companies (who can borrow against your portfolio) and lazy financial advisors (who can charge management fees for essentially doing nothing) AT YOUR EXPENSE.

Click here to schedule a free no obligation consultation with our Fee Only Fiduciary Financial Planning team.

How Big Finance Benefits When We Use Strategic Asset Allocations

We call the “Wall Street, Government, Media” partnership tripod “Big Finance”.

This is because over the past 50 years they have colluded together to increase their economic benefit at the expense of ours, the individual consumer.

Big Finance makes its profit by holding your money.

They lend against your investments, or they charge fee’s for holding the investments, or both.

Therefore, it’s in their best interest to convince you that leaving your money in one place in one format for long periods of time is in your best interest!

On the one hand, Big Finance tells us that investing is simple, that we should use buy and hold, strategic asset allocation investment strategies because history is our guide.

At the same time, Big Finance uses industry jargon, complicated paperwork, and an ever-expanding complicated investment universe to the convince you to have one of their corporate financial advisors manage that “simple buy and hold strategy”.

Big Finance wins either way.

Whether you buy into the fact that investing is simple and manage your own buy and hold strategy on your own, Big Finance profits.

Or if you delegate your retirement portfolio management to a fancy looking suit wearing corporate investment portfolio manager, they charge management fees and profit there.

The issue we have with this system is that Big Finance is not rewarded based on better retirement outcomes!

They are rewarded regardless of whether you as the retiree have better retirement outcomes or not.

Click here to schedule a free no obligation consultation with our Fee Only Fiduciary Financial Planning team.

Additional Areas Asset Allocation Falls Short

Asset allocation alone does not tell us enough about how we should properly invest our retirement money.

First, it falls short in the sense that it is a categorical guide not an actual investment specific guide.

This is a major failing that goes unexplained…

Second, asset allocation tells us nothing about that investments BETA (sensitivity to the overall investment market), Standard Deviation (statistical result range), or historic Maximum Drawdown.

These are key pieces of information that should guide ones investment selection.

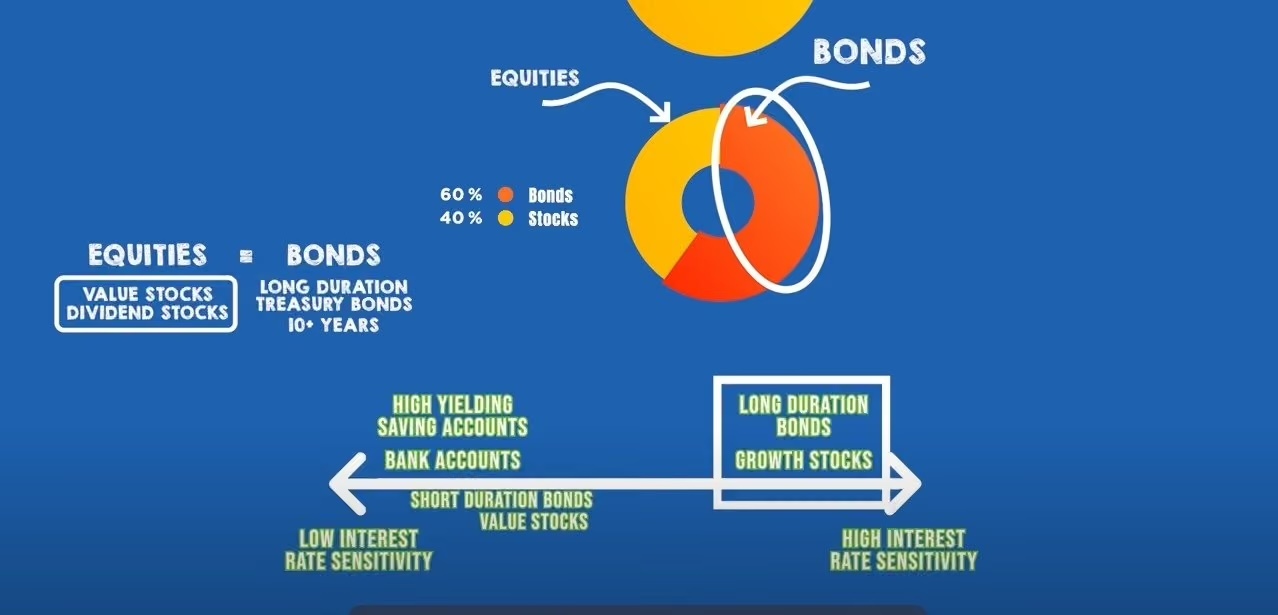

Third, asset allocation tells us nothing about an investments interest rate sensitivity.

Fluctuations in interest rates have a profound but predictable effect on a range of investment types.

For example, bond prices go up when interest rates go down, and bond prices go down when interest rates go up.

This effect is more exaggerated the longer the maturity of the bond (meaning that for 3 month bonds this effect is minimal but for 30 year bonds this effect is extremely powerful!).

This relationship is also true for certain types of stocks!

Growth stock (especially small cap) prices generally go down when interest rates go up, while their prices go up when interest rates go down!

Knowing this, one would (correctly) summarize that growth stocks and long maturity bonds are actually influenced VERY SIMILARLY.

One would also (correctly) summarize that holding long maturity bonds does NOT actually diversify (reduce risk) in your retirement portfolio!

This is just one simple example of how interest rate sensitivity should be factored into the investment selection within your retirement portfolio!

What We Believe

At Peak Financial Planning, we won’t mince our words.

We believe that investing for retirement is COMPLICATED.

We believe that it is a profession just like any other - one that takes years of education, experience, and trial by fire to master.

If someone told you that you could open a business and succeed at it with 2 hours a year invested over 30 years, you would laugh.

Yet that’s the propaganda you are being fed - that with minimal effort you can have your (investment) cake and eat it too (when that is not true IN ANY OTHER AREA OF YOUR LIFE).

We believe that the average consumer (you) is far better served focusing on the behavioral decisions they can control (like building a comprehensive financial plan!) rather than investment decisions that they are not an expert in.

By focusing on things like how much you spend, how much you save, maintaining your health, planning for social security, you can actually have a material, controllable impact on your income in retirement (We have an entire FREE webinar course dedicated to teaching this subject, you can also view a Sample Financial Plan here).

Click here to schedule a free no obligation consultation with our Fee Only Fiduciary Financial Planning team.

FAQ

What is an asset allocation?

Asset allocation guides your portfolio's weighting towards different asset classes with two main choices. Strategic asset allocation is a longer term strategy that considers longer time periods for tactical strategy changes. The target allocations will stay the same and may need to be rebalanced. Rebalancing involves the trades necessary to bring your portfolio weights back to where they should be. Tactical asset allocation decisions are a method of using shorter term shifts to adjust based on market volatility. This is changing your goal allocations, not rebalancing back to the original plan.

What are Asset Allocation Funds?

Asset allocation funds center their strategy around a standardized asset mix that often doesn't account for your needs. The allocation is usually a basic portfolio to minimize the work needed for your investments. Basic funds often come when you have a simple service like a Robo-advisor. Active portfolio management should not fall into this category but it often does.

What is a Target Date Fund

Target date funds change the asset allocation as you near a set time that you determine. Often people select their time horizon to line up with a big expense, such as desired retirement or a child's college start year. As you near the target date, the various asset classes shift from riskier to more conservative. This is supposed to help get you more money when you need it.

What is a Three Fund Portfolio

There is a growing movement, saying we don't need many positions, especially individual stocks. The argument is that index funds are naturally diversified, so we can use say a 3 fund portfolio. This strategy would have 1 stock fund, 1 bond fund, and 1 international or emerging markets fund. Ideally allowing us to accomplish what a more complex portfolio would have done.

We don't believe that this is an option. Investors have very specific needs for portfolio based decisions. You can watch a video we made on this here:

What should I use to determine my investment strategy?

More important factors besides plain asset allocation include interest rate sensitivity, portfolio income vs growth, and the goals for your assets as they relate to your financial needs.