Retirement Planning's Missing Phase - Don't Ignore This!

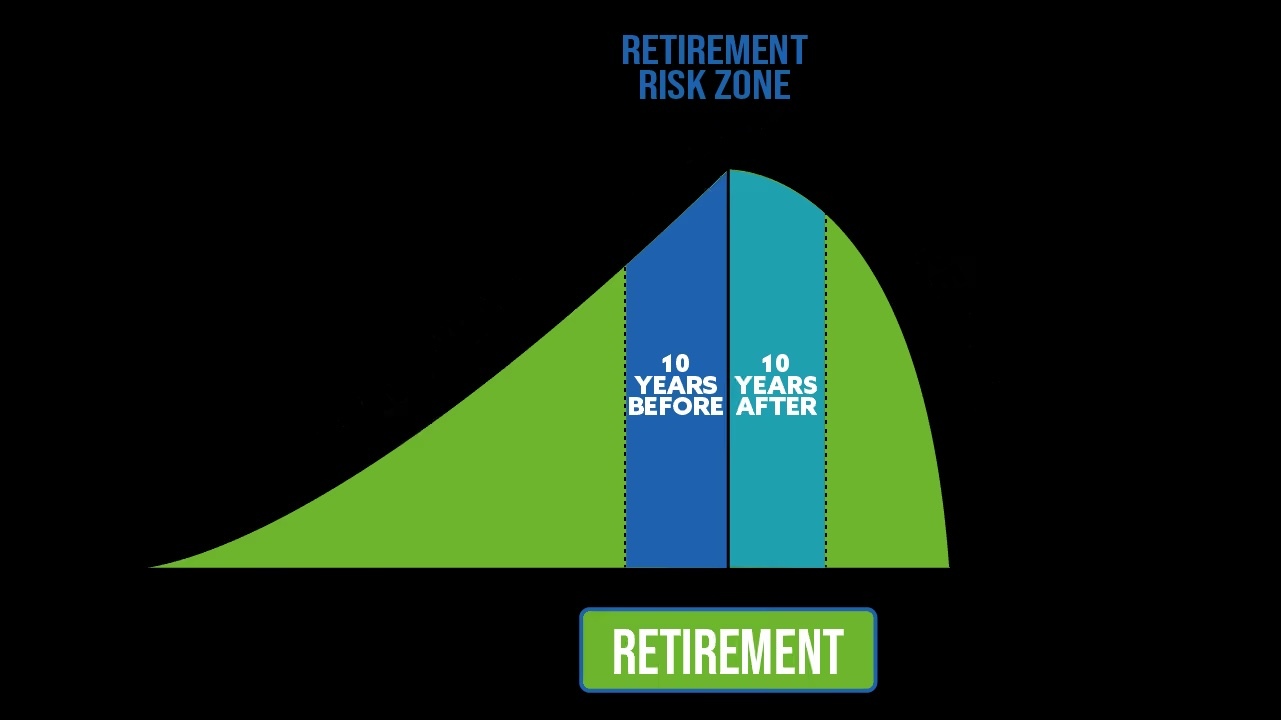

Retirement planning is often broken down into 2 phases: accumulation and distributions. Yet there is a gap in most planning. The third critical period is called the retirement risk zone. We focus on this forgotten third phase which constitutes the ten years before and after retiring.

The retirement risk zone is where you will face many obstacles that create stress or financial burden. This article will help clarify what to watch for, how to judge your own financial picture, and how to measure your own success.

Peak Financial Planning specializes in helping people in the retirement risk zone conquer their financial risks. These topics will be analyzed through the lens of our actual planning process that has helped over 30 retirees fulfill their retirement dreams.

Table of Contents

- The 2 Phases of Conventional Retirement Planning

- The Missing Phase of Retirement Plans - the Retirement Risk Zone

- Cash Flow Planning During the Retirement Risk Zone

- Retirement Income Planning During the Retirement Risk Zone

- Tax Planning During the Retirement Risk Zone

- Bringing it All to a Close

- FAQ

The 2 Phases of Conventional Retirement Planning

Most people see retirement as just two phases: accumulation then distribution. Growing wealth and then spending it down.

Neither the accumulation nor distribution phase can be overlooked because both have significant impact on retirees. We will cover these two phases before exploring the missing third phase with the most risks.

The Accumulation Phase

The accumulation phase consists of your working years, more specifically when you begin to save and build wealth. This is the time to build an education alongside your savings.

The problem is that most people consider retirement an abstract and distant puzzle that doesn't enter line of sight until you are actually leaving the workforce. Traditional planning creates a blind contribution system that doesn't involve education.

You don't need to become an expert in day trading and IRS tax rules regarding savings plans but you do need to understand what works best for you. For example, how much your employer will match in contributions or what accounts to contribute to.

You typically see X percentage of an investor's salary going to a 401k or IRA from each check they receive. You not only need to save but you need to learn what you invest in and how it benefits your retirement goals.

The Distribution Phase

The distribution phase is when you leave the workforce and begin to draw from your savings.

This should be a peaceful time where you can relax and enjoy the benefits of your hard work. Unfortunately, few people practice careful planning until they're confronted by a swirling pool of decisions and questions that feels overwhelming.

How much do I have in portfolio assets? Where will I take distributions first? What are the tax consequences of each distribution? How do I navigate market downturns? These are just some of the questions that affect retirees.

Many scramble to find help through a financial advisor just before or after retirement. However, many advisors focus on churning fees and pushing an agenda that only benefits them, not the client.

If you find yourself in this crisis, you can reach out to Peak Financial Planning.

We are a team of fee only, fiduciary financial planners that are legally obligated to act in your best interest.

The Missing Phase of Retirement Plans - The Retirement Risk Zone

What most people do not consider are the years surrounding retirement. Some may avoid retirement planning out of fear or even ignorance, but this only harms you. It's ok to not know everything pertaining to savings, distributions, and taxes. But you will want to learn what you can before your retirement date.

When it comes to retirement what matters most are the years immediately before and after you've retired. This is because you have to account for the behaviors and income stream that will influence your new lifestyle.

Why the Retirement Risk Zone is the MOST Important Phase

The crux of the retirement risk zone is that you can’t go back in time. If you haven’t properly planned, you can be trapped in a position of fear and stress. One way this can manifest is you attempt retiring and then find yourself working a part time job because you’re unable to support your needs. The uncertainty of how much you spend, how much you need to earn, what’s happening with your retirement savings, and what you can and can’t afford will obstruct your life.

If you take the time to understand your perspective and how you behave with money, you can build a solid foundation for your financial future. Knowing what you are comfortable with and how you spend can create success. For example, understanding how much cash you need to feel safe, or your satisfactory quality of life creates a stable baseline.

In the retirement risk zone you are likely at the peak of your overall wealth. You need to understand where your wealth is coming from, where it goes, where it is allocated and how to withdraw it.

In the 10 years before retiring, you are likely earning the most that you will earn in your lifetime. You’ve had many years to build your career. By the time you reach full retirement age you have high income, likely with higher spending habits to match. Many seek to increase their quality of life once they stop working. This requires an understanding of your cash flow.

Many people also save the most during their last 10 working years. This often accompanies the higher salaries that people experience towards the end of their career. You should be saving what you can afford to if you don’t have substantial savings built up for your new chapter of life.

Cash Flow Planning During the Retirement Risk Zone

As you get older you will want to start looking towards when you can retire. People often get distracted by conversations about investing, such as their portfolio value and strategies to grow their wealth. These are useful tools that can help you. But they are only useful in terms of optimization. Before we can optimize your plan, we need to make sure that you are stabilized. Stabilization comes from understanding your cash flow.

Developing a tracking system that keeps you accountable enables you to understand your spending. There may be some shame around this process and that is a natural response. However, it is necessary to reconcile estimated spending with real numbers. A red flag in your financial professional is that they shame you, rather than encourage you.

Here is a link to our expense tracking worksheet that can help you break down your spending if you are unsure of where to start.

These are examples of some common categories of spending we see with our clients.

You will want to differentiate between your necessities and your discretionary expenses. Doing so allows you to calculate your individual needs and what dials you have available to tune.

Once you have actual spending details, you can project your spending after retiring. You may plan to live modestly. Maybe you have plans for travel and excitement. These are both plans and things can always change, but they're necessary to develop so change doesn't hinder your success. A major benefit to look forward to is that you will confidently know what your cash flow looks like. Additionally, you will also be able to set real goals for yourself.

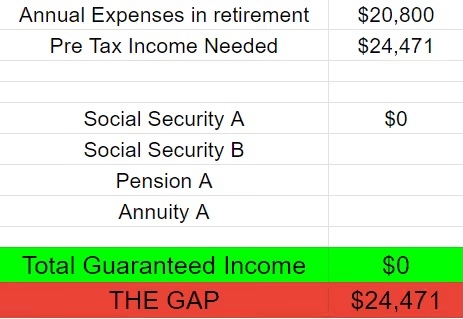

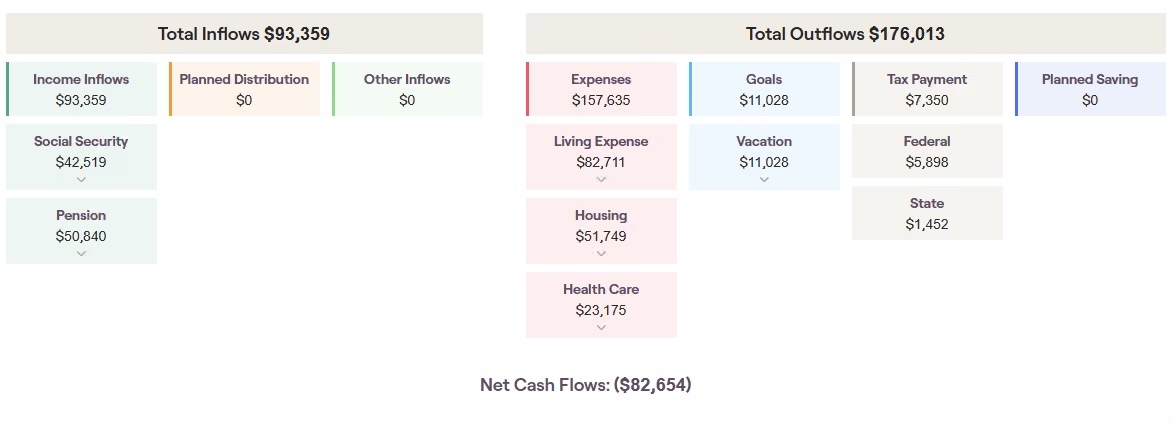

After developing a stable projection of your guaranteed income (think Social Security, Defined Benefit Pensions and Annuities) compared to your spending in retirement, you are able to estimate your required portfolio income, or RPI. Your RPI is the difference between what you'll earn from guaranteed income and what you will spend, by choice or constriction.

Here we see net and gross income needed. We then list out guaranteed income sources. The RPI is "the gap" that you have to make up if you will spend as much as we plan for.

Whether you have a conservative lifestyle or live more comfortably than during your working years is up to you. You will need to know what is available based on what you can afford. Can you increase spending? Do you need to decrease spending? Will you have to work longer? Should you defer Social Security payments to increase benefits? This is where cash flow planning fits into the equation and you can't answer these questions without understanding your cash flow.

Retirement Income Planning During the Retirement Risk Zone

Income planning comes after accounting for cash flow and calculating your RPI. This also helps determine when you can retire.

For example, you plan to spend $6,000 per month after you retire. Your pension is guaranteed to give you $36,000 a year. You also have Social Security which will pay you $1,300 per month.

You first want to match annual or monthly amounts to make everything digestible. So, let’s use monthly totals. Your spending is expected to be $6,000 per month. Your Social Security is also given as a monthly $1,300. Your $36,000 per year pension gives $3,000 per month. Earnings are $4,300 per month. Spending is $6,000 per month.

You can see that there is a substantial gap between what you will earn and what you want to spend. You have three options from this point:

- You can work longer.

- You can cut back your retirement lifestyle by living in a cheaper location, spend less on discretionary items, or seek out support from family and friends.

- Your last option is to take the required income gap from your portfolio.

You know that you need to earn an extra 1,700 per month. Best case you start early and plan well, so you will be able to comfortably draw money from investments.

Investor Goals

Ideally you have investable funds that can work towards your goals. The three forks of investing are growth, income and safety. Picture a triangle with each objective at separate corners of the triangle. The closer you get to one point, the further you get from the other two.

You can try to pursue high rates of return and grow your portfolio's value. This means greater risk in terms of market risk and specific risks tied to your chosen investing vehicles. More risk, more return. This is where sequence of returns risk matters when planning for distributions.

You can also choose stable cash inflow. This would open you up to two retirement risks that are very common. Inflation risk means that your investments may not generate enough return to outpace inflation. Keep this in mind when relying on an especially conservative strategy such as holding only cash. An annuity is a demonstration of this risk. Fixed annuities do not increase their benefit amount as the cost of living rises.

You can choose preservation of value so that you can leave money to your spouse or heirs. You may also temporarily shift your asset allocation for more downside protection, using preservation of capital to hopefully lower the drops in value.

A good financial plan helps retirees avoid inflation. Unfortunately, most financial advisors only do this through asset allocation. But you will need to understand that not some stocks may act like bonds, and vice versa. The same can be said for funds concentrating in stocks or bonds.

Another risk attached to cash flow goals is interest rate risk. If interest rates go down, you can't reinvest your interest payments at the same rates you originally did, which will mean lower income from investments purchased using those payments.

Your risk tolerance and personal goals will determine which path you take. Your financial situation dictates the monetary risks you can tolerate as an investor, but you also need to consider your psychological appetite for risks. Individual personality will determine what you are willing and able to tolerate in terms of risk, in the form of loss of value.

No matter how well your retirement plan is crafted you will need to have at least one backup plan that is catered to your specific needs and objectives. This may end up being a sizable amount in a savings account or a well-suited investment strategy in case the market significantly drops. Your family should make thorough plans for hard times, so that you are ready, but hopefully never need them.

No matter who you are, you're susceptible to one of the biggest risks in retirement, called "Sequence of Returns". How does sequence of returns risk affect you? The return risk can be demonstrated when you face market downturns, reducing your net worth. This happens while you're taking distributions exponentially reducing your total asset pool. This means you need increased rates of growth in the following years to hit break even.

This is one of the most ignored problems on behalf of the retiree community amongst negligent advisors. Return risk can't be ignored during your most crucial years, which are often between retiring and claiming social security. Often times, you may be struggling to produce enough money to sustain your nest egg during this period. This is a time when drawing more money than necessary can ruin your success rate. Further increasing the need for correct withdrawal strategies.

Distribution Planning for the Retirement Risk Zone

To combat risks like sequence of returns, you need a suitable distribution strategy. Many traditional methods do not take into account individual goals and needs. They also skip over some glaring risks like sequence of returns risk. This is most obvious with methods like the 4% rule that do not adapt to change.

The 4% Rule

The 4% strategy says if you withdraw only 4% of your portfolio's value every year you will never deplete the value of your investments. This works great if your portfolio is of substantial size, and most importantly, the market is guaranteed to have high rates of return every year.

What about retirees who don’t have significant wealth in investments? What about market downturn year over year? Our point can be demonstrated with the following example: We start with the same portfolio value and withdrawal rates.

As you can see here, the static 4% withdrawal rate ends up with drastic differences in ending wealth if you have the same yearly returns as a group but start out with negative years. Negative returns combined with withdrawals lead you to end up with much lower portfolio value over time. Even if using the 4% rule here implies we will never fully draw all of our assets (not guaranteed) you end up with nearly half the value.

Pro Rata Distributions

Pro rata distributions are another common strategy where you sell the same amount of each asset to make the withdrawals even. For example, you own 4 stocks and they each make up 25% of your total portfolio. When you want to withdraw 4% of your total stock value, you will sell 4% of each stock, to make this happen.

The issue here is that you aren't accounting for indvidual positions. You can end up with taxable proceeds you were unaware of. You may sell securities that are not performing well, without giving time for rebounds. You could even sell off assets that you need in order to produce required income.

Neither of these methods are suited to your individual situation. They will inevitably leave you shorthanded and wishing that you had a tailored strategy for distributing your portfolio. The best method by far is a dynamic distribution strategy that accounts for your unique circumstances.

Here is a distribution strategy that makes more sense for a retiree that has some, but not significant spending flexibility:

Floor and Ceiling Spending

You can create guardrails on spending which follow your investment performance, with more spending in growth years or less spending during market downturns. This approach is called the "floor and ceiling" strategy.

If you have the means to, you can plan on spending less, so you take less money out of your portfolio. This helps mitigate the sequence of returns risk.

The guardrails are typically a percentage increase or decrease from your average spending. For example, you spend $4,500 per month, and the market goes down 10%, you can decrease spending by about $450 per month, so that you don't over withdraw. Should your portfolio's value increase by 10%, you can increase spending by $450 per month.

Most financial advisors will not give you a proactive plan that helps course correct before your plan is catastrophized. This is why you benefit substantially from training and education on investing and distributions, or a qualified financial advisor who has your best interests at heart.

Tax Planning During the Retirement Risk Zone

Your largest expense in retirement will be taxes. Tax planning is one area that you need to take advantage of should your plan be in an optimization state. There are a few options to reduce your taxable income.

Roth IRAs and Conversions

The first option is more viable the earlier you start. You can start to fund a Roth IRA for nontaxable distributions. Roth IRAs will enable you to withdraw your money, fully tax free, if you are over age 59 ½ and have had the account opened for at least 5 years before withdrawals.

Another option is Roth conversions. Roth conversions are when you deposit savings into a Roth plan that were originally pretax, deductible contributions. This means dollars from any traditional IRAs, 401k’s, 403b’s, and any other pretax contribution plan or annuity. Because you deducted contributions in these mentioned plans, the IRS charges tax on those contributions converted. The full conversion amount is added to your ordinary income, and taxed as such, for the year converted. The 5-year timer will start the day you initially start your Roth account.

The tradeoff here is that you will shift the tax liability from your future self to the present year. Should you be able to afford this extra expense now, you will have less tax in the future. This is another strategy that would be ideal should you have runway time before needing the funds, and the spending flexibility to fund your current lifestyle.

Roth conversions have a breakeven point, that requires living longer than the time period which creates a financial increase in your net worth. This is typically several years beyond the actual conversion.

You also want to consider what type of accounts you own. The benefit of taxable accounts is simplicity; there are no rules to remember. However, you lose the benefits of tax-deductible contributions and tax deferral on withdrawals.

IRMAA and Medicare

Another factor to consider is something called IRMAA surcharges on your Medicare premiums. IRMAA stands for Income Related Monthly Adjustment Amounts, affecting the amount you pay per month for Medicare Part B and D premiums. When your income is above a certain threshold you will have to pay a set amount of IRMAA surcharge in addition to your premiums. Both also get increased every year for inflation.

The catch is that IRMAA surcharges for a given year are based on your income from two years prior. The only way to avoid this is to reduce your taxable income. Ideally, this will be reorganizing your assets into tax free withdrawals before you need Medicare.

Bringing it All to a Close

The retirement risk zone can be harsh and daunting. Fortunately there are steps you can take to protect yourself, and even thrive in successful retirement. The earlier you start the earlier you are in control of your plans. You can only be too late if you never get started. While the work may feel difficult at the moment, it will pay off multiple times over when you can reach retirement age and enjoy the fruits of your labor. Organizing the steps you need to take will enable a digestible action plan to be created.

Click here to see a comprehensive sample financial plan.

First you must understand where you are in proximity to your goals by gathering an accurate picture of your current situation. This requires accounting for what your finances look like right now. You will want to obtain your financial documents, and sort through all of your assets and obligations. Once you have a clear grasp on where your net worth we can move on.

The second part of the plan is understanding your specific retirement risks by detailing your current and expected cash flows. You will want to know how much you are earning from any current sources of income. Next you think about how much you expect to spend after retiring. The amount of cash flow coming in and going out will help determine how close you are to your goal of retiring.

Next, you have to account for any missing gaps in income. That can come from a myriad of sources, but if you plan to spend more than you make, it has to be accounted for. If you have the means to provide for yourself, hopefully you will have retirement savings to fill income gaps with liquid assets.

This creates a series of nested decisions based on the forks in the road. We must account for tax and distribution strategies. Hopefully you or your financial professional will be knowledgeable in navigating the mechanics of investing and distributions. An uneducated or confused investor can drain their retirement savings without accounting for taxes and investment performance.

FAQ:

1. How do I start planning for my retirement?

Starting to plan for retirement means breaking down your current situation, your cash flow plans, and retirement income plans. Each step has a checklist that you can follow. The very first step is understanding where you are in terms of financial security at this current point in time.

2. When can I retire?

The decision of when you can retire depends on your cash flows, and your assets available to support any needs you may have. Cash flow planning is a prerequisite for getting to this stage.

The simplest form of the equation is:

Guaranteed income + investment income - expenses in retirement = required dollars

3. Can I afford to retire?

Whether or not you can afford to retire depends on the above equation. You must calculate the estimated amounts of income from guaranteed sources (Social Security, Pensions, etc) and what your portfolio will be able to support and then adjust the retirement spending accordingly.

4. How can I avoid taxes in retirement?

The best ways to reduce taxable income are tax free sources like ROTH IRA’s, having long term capital gains, or more complicated strategies such as tax loss harvesting.

5. How do I take distributions in retirement?

Taking distributions in retirement will be a crucial part of your success. The best way to take distributions is by using a dynamic strategy that adapts to your individual situation. No blanket rule will serve you well for your entire retirement.