Annuities have been a core piece of the retirement puzzle for many investors. But what is the primary reason for buying an annuity as opposed to other investment options? The answer: guaranteed income. For investors that are nervous about the future financial landscape, an annuity can provide peace of mind by ensuring a guaranteed stream of income throughout retirement.

In this guide we will cover the various types of annuities and how they work. We'll discuss the tax advantages they offer and how they can help diversify your retirement portfolio. We will discuss how annuities allow you to offset your investment selection risk and shift that onto an insurance company - relieving you of the burden of figuring out where and what to invest in. Finally, we'll cover costs and fees related to an annuity purchase as well as how to compare annuities against other investment options you might consider in your retirement portfolio.

This guide is not designed to recommend for or against the purchase of an annuity. It is simply designed to educate and inform you of the considerations when evaluating whether to add an annuity to your retirement mix.

We help individuals and couples navigate the retirement risk zone (10 years prior to retiring and first 5 years in retirement). If you like what you read in this guide, schedule a free consultation with us to learn more about working with our fee only, fiduciary financial advising team.

An annuity is an insurance contract designed to provide a guaranteed stream of income in exchange for a fee. Annuities are especially appealing to investors concerned about:

1) Outliving their savings

2) Volatility of traditional investments such as stocks, bonds, ETFs, Mutual Funds, Real Estate, or Businesses

Annuities are one of the most stigmatized investment vehicles in the retirement planning space.

This is because the annuity industry is rife with conflicts of interest, unsavory sales representatives, and misleading contracts.

Understanding the various types of annuities, how they function, and the costs and trade offs associated with them is CRITICAL.

The first, and most important thing to understand is that annuities are offered for sale by life insurance companies.

Any licensed financial professional that sells annuities does so on a commission basis and therefore cannot be considered a fiduciary (for more information on the importance of your financial professional being a fiduciary, click here).

That being said, annuities can be suitable and should be considered by certain investors in certain cases.

At Peak Financial Planning, it is our belief that any annuity purchase should be considered and evaluated by a Fee Only Fiduciary Financial Advisor who is free of the conflicts of interest that the annuity sales person faces.

If you are evaluating how an annuity may fit into your retirement plan, click here to schedule a free consultation with our Fee Only Fiduciary financial advisor team.

In exchange for an initial investment, an annuity provides a series of periodic income payments. These payments can be tailored to meet your specific needs, such as providing a fixed or variable income stream and offering different payment durations and continuation options. Some annuities even include a death benefit (similar to life insurance), which can provide an added layer of financial protection.

Understanding how annuities work and the benefits they provide is crucial when considering whether an annuity is a suitable investment vehicle for your retirement needs.

There are hundreds of nuanced annuity products available.

When an annuity contract pays out, how much it pays out, and for how long it pays out are all variables that will be addressed in the annuity terms.

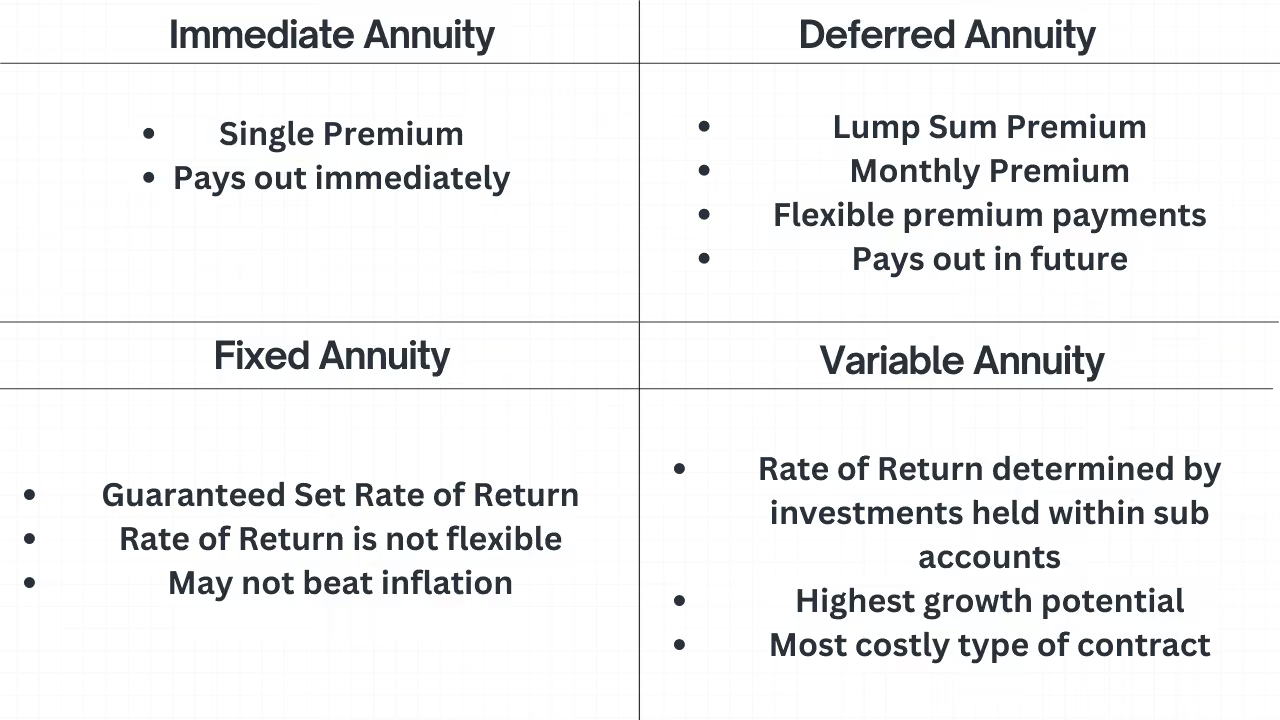

Immediate annuities begin paying out immediately after the contract is purchased. They provide a fixed dollar payout guaranteed for life that you will be able to identify in advance of purchasing the contract.

The tradeoff here is that you trade guaranteed income in exchange for liquidity. Once the contract goes into effect, you will not have the option to access your invested funds in a lump sum were you to need it for emergencies. If you do choose to try to access your original invested amount in a lump sum, there will often be fees or penalties applied, and you will only be able to access a limited amount.

Deferred annuities pay out at a future date. They provide guaranteed income in either lump sum or monthly income payments, depending on the annuitization option the investor chooses.

Payments INTO the annuity can be made flexibly - either as larger lump sums, or as monthly premiums. The insurer who guarantees the contract invests the funds on your behalf which offers the opportunity for your principal (original invested amount) to grow before initiating payments.

One big advantage of a deferred annuity is the ability to contribute funds on a tax-deferred basis which allows the funds to grow without being taxed UNTIL you withdraw money. There are no annual contribution limits being placed upon deferred annuities (unlike IRA's and 401(k)s).

Deferred annuities have up front fees, surrender fees, and ongoing fees for contractual elements such as riders. We will review how annuity fees work down below.

The "fixed" in fixed annuity refers to the interest rate (or growth rate) guaranteed in your contracts terms. A fixed annuity has a fixed growth rate that is set for a pre-defined period of time (guarantee period) in the contract.

At either the end of the contract or the end of the guarantee period, you can choose to annuitize the contract (begin receiving income payments) or to renew or transfer your invested money into another retirement account or annuity contract.

With fixed annuities your interest rate (rate of return) is not impacted by market volatility. In most cases this means during good market years you will receive a lower than market rate of return, and on bad market years you will receive a greater than market rate of return on your invested money. The big risk here is that the fixed interest rate may not keep up with inflation and underperform alternative investments.

The "variable" in variable annuity refers to the interest (or growth rate) available. The variable annuity will afford the greatest growth potential of the different annuity vehicles.

Money can be invested into the contract in either lump sup or monthly premiums which are then invested into "sub accounts". Sub accounts are mutual funds whose investment performance varies depending on market risk and market performance.

Variable annuities are the most complex of the annuity products and should be evaluated with care. Because they can be modified and customized in an almost unlimited manner, they can be extremely expensive and, in some cases, predatory.

At Peak Financial Planning, we do not sell annuities and are therefore free of the conflict of interest of receiving a commission for recommending it as a part of your retirement portfolio. If you are evaluating how an annuity may fit into your retirement plan, click here to schedule a free consultation with our Fee Only Fiduciary advisor team.

The primary reason for buying an annuity is for the guaranteed payments in retirement. This guaranteed retirement income, can help mitigate the risk of outliving your savings and ensure you have a steady income stream in retirement.

Lifetime income refers to a consistent stream of payments guaranteed for the duration of your life. Lifetime income is provided even after your initial contribution has been expended. This means that if you live longer than expected, your annuity will continue to provide you with income, helping you avoid outliving your savings.

The primary advantage is the peace of mind lifetime income provides. However, there is risk that income annuity payments may not adequately keep pace with inflation or that you may not receive the full value of the annuity if you pass away before all payments are made.

Longevity risk refers to the potential of outliving your financial resources. This risk is amplified by the increased life expectancy of individuals at retirement age. Annuities help mitigate longevity risk by offering guaranteed payments for life.

Just remember - annuities cost money in exchange for the lifetime guarantee. You must make sure the fee you pay produces an amount of income substantial enough to support your retirement needs.

In addition, you must feel very secure with the insurer insuring the annuity insurance contract. If the insurer were to face financial difficulty or go out of business while you are still alive, you run the risk of losing the guaranteed payments.

Peak Financial Planning is an independent Registered Investment Advisory practice. We do not sell annuities or work for/partner with any insurance companies which allows us to remain conflict of interest free when evaluating annuity contracts. If you are evaluating how an annuity may fit into your retirement plan, click here to schedule a free consultation with our Fee Only Fiduciary advisor team.

Annuities offer potential tax advantages that can help you maximize your retirement savings. Tax-deferred growth means that your investments within the annuity can grow without being subject to taxes until you withdraw the funds.

Additionally, the tax treatment upon withdrawal depends on whether the annuity was purchased with pre-tax or post-tax dollars, which could result in potentially lower taxes on your income.

For example, annuities purchased with pre-tax dollars are subject to full taxation upon withdrawal, while those purchased with after-tax dollars are only taxed on the earnings.

Tax-deferred growth is an investment strategy that allows your money invested to grow without being subject to taxation until the time of withdrawal. This means that the interest, dividends, and capital gains earned within the annuity can compound more quickly than they would in a taxable investment account.

The primary advantage of tax-deferred growth is that it enables you to postpone taxes on your investments until they are withdrawn, potentially enabling you to grow your investments at a faster rate than if they were taxed annually. Furthermore, tax-deferred growth can assist in reducing your overall tax liability, meaning you create more investable money over time.

The tax treatment upon withdrawal of an annuity depends on whether it was purchased with pre-tax or post-tax dollars. If the annuity was acquired with pre-tax funds, all withdrawals of any generated earnings on the contributions are subject to full taxation. However, if the annuity was purchased with post-tax funds, taxes are only paid on the resulting earnings, allowing for potentially lower taxes on your income.

In the case of individual retirement annuities and ROTH IRAs, mandatory distributions are only required upon the individual's passing, providing additional tax benefits. Understanding the tax implications of an individual retirement annuity is crucial when considering this investment vehicle.

You can speak with our Fee Only Fiduciary advisor team if you have questions about potential tax advantages or implications regarding an annuity you are considering or own.

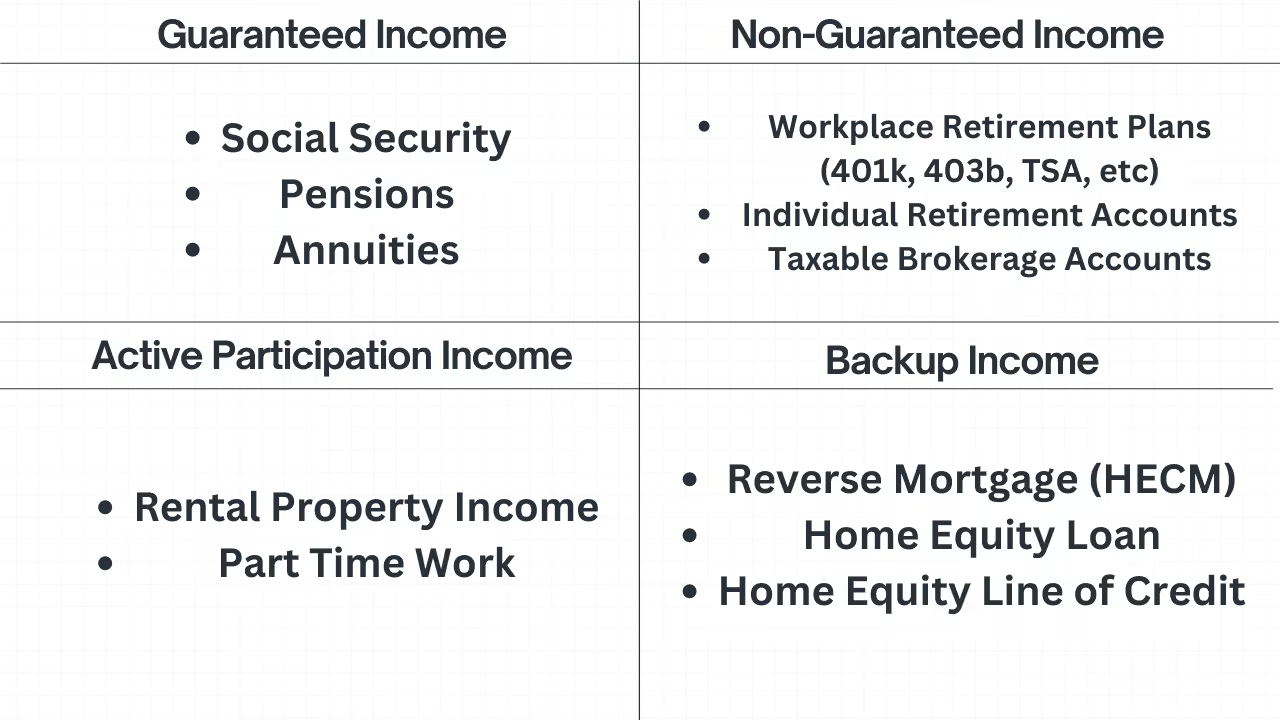

An annuity can provide an additional source of guaranteed income in retirement. Most of us will have Social Security as the only source of guaranteed income in our retirement. In some cases the fees and expenses related to an annuity purchase may warrant adding one to your retirement portfolio.

Annuities function similarly to bonds or bond funds in that they reduce risk in your portfolio. In most cases the invested value of an annuity is much less volatile than the broader stock market. And, because it provides guaranteed income payments similar to a bond, it can be thought of as the fixed income or bond portion of your retirement investments.

Annuities reduce volatility and provide stability to your financial plan. The income is guaranteed and can be used to fill income shortfalls left if social security or pensions are not sufficient.

In exchange, you give up legacy value that your heirs would otherwise inherit were the money invested in more traditional investments such as stocks, bonds, mutual funds, or ETFs.

In nearly all cases, at the end of the annuitant's life (the annuity owner or beneficiary) the contract ends and whatever invested value remains in the annuity contract is forfeit to the insurance company.

Before purchasing an annuity, it's essential to consider the fees, expenses, and restrictions one might face when investing in an annuity contract.

Annuity purchases often come with hefty up front sales fees that can range from 1%-8% of the annuity purchase price. This means that a $100,000 single premium deferred annuity with a 6% up front fee leaves the investor with $94,000 invested - not the $100,000 one might think.

For reference, many ETFs, Stocks, and Bonds have no upfront fee. Mutual funds may have a 1%-4% upfront fee. Real estate usually has a less than 1% upfront fee for the buyer. You can see that annuities are relatively expensive.

Annuity up front fees are usually among the highest of all investment options available in the investment marketplace because the cost to provide guaranteed future payments is so high for the insurer.

Annuities also have ongoing fees. These fees can include "mortality and expense" fees (1%-2% per year), rider fees (hundreds of dollars per year), administrative fees, and subaccount expenses (.1%-1% per year). Again, it is critical to get a handle on what an annuity will cost as the fees and expenses can rack up and eat away the potential benefits it might otherwise provide.

Most annuities are not liquid - meaning you, the annuity owner, cannot regain access to the original invested money without paying penalties. These penalties are called "Surrender Charges". Surrender charges start out higher in the early years of the contract and go down year by year until they eventually drop off entirely. Depending on the contract, surrender charges can be in effect for as long as 15 years. You should ALWAYS make sure to ask about surrender charges and fully understand the penalty amount and duration before purchasing an annuity.

For the small range of annuity contracts that do offer legacy options, heirs may be taxed inefficiently. Heirs cost basis on an annuity are based on the original purchase price of the contract. All gains above that original purchase price are taxed at ordinary income tax rates and must be paid immediately upon the heir taking possession. Were your money invested in more traditional investments - taxable accounts, IRAs, etc - heirs would receive either a step-up in basis or have a more extended period of time during which to withdraw money and therefore spread out the tax burden.

When deciding if an annuity is right for you, it's crucial to assess your financial goals and retirement needs. Consider the amount of income you desire in retirement, the length of time the annuity will be held, and the amount of risk you're willing to accept. A certified financial planner can help you evaluate your financial situation and determine if an annuity is a suitable option for meeting your retirement goals.

Click here to schedule a free consultation with one of our fiduciary certified financial planners.

Because annuities can be prohibitively expensive and complicated, it is important to consider alternative investments before committing to an annuity purchase.

Mutual funds and ETFs are popular alternatives to annuities. Mutual funds and ETFs provide diversification, exposure to a broad range of asset classes and niche markets, and tax efficiency. ETFs tend to be more tax-advantaged than mutual funds and usually have lower fees, while mutual funds provide specialized portfolio management.

Real estate and dividend stocks can provide income and diversification. Real estate investments offer greater flexibility in terms of investment options and can generate an additional source of income through rental property. Rental real estate is a business however, and should be evaluated carefully.

Dividend stocks, on the other hand, offer the potential for higher returns than annuities and can provide a steady flow of income through dividend payments. They are also more liquid and do not come with the myriad of fees that may come with an annuity.

Click here to schedule a free consultation with one of our fiduciary certified financial planners if you'd like to learn how some of these other investment options may fit into your individual retirement and plan.

.avif)

Annuities can be a valuable tool in your retirement planning arsenal, offering guaranteed income, tax advantages, and the potential to diversify your portfolio. It's essential to carefully consider factors such as your financial goals, retirement needs, risk tolerance, and investment time horizon, as well as the fees and expenses associated with annuities before making a decision.

Click here to schedule a free consultation with one of our fiduciary certified financial planners.

Common examples of an ordinary annuity include periodic loan payments, such as mortgages and car loans, which are made at regular intervals over the life of the loan.

Interest payments on bonds are also an example of an ordinary annuity, with payments made according to pre-determined term length and payment frequency.

The key difference between an ordinary annuity and a regular annuity is when the payments are due. An ordinary annuity has payments due at the end of each period, while a regular annuity has payments due at the beginning.

An ordinary annuity is used to save for retirement or provide a steady source of income. It involves making regular payments over an established period of time, which can be received monthly, quarterly, or annually.

Ordinary annuities come in two varieties: immediate and deferred. An immediate annuity begins payments immediately after the initial premium payment, while a deferred annuity delays payments until a set date in the future, such as upon retirement.

The main purpose of buying an annuity is to provide a guaranteed source of income for retirement. They are especially useful for those who are concerned about outliving their savings.

Free on-demand training

How to retire knowing nothing was missed.

✓

When do you have enough saved?

✓

How much can you spend?

✓

How do you pay the least taxes possible?

►

.webp)

.webp)

.webp)