Should you use a Model Retirement Portfolio?

Portfolio management can be daunting for any investor. There are multiple nested decisions for each action that you take. For example: which models do you use? Do you invest in stocks or bonds? Where do you find model portfolios? How do you consider market conditions? Should you work with a financial professional? Out of a myriad of investment companies, which one do you work with? How do they come up with their models? What is portfolio rebalancing? How often should you rebalance your portfolio?

Models are one way to simplify investment management and can help you achieve your objectives. A model portfolio is a collection of one or multiple strategies that comprise your overall investment strategy. Just about everyone uses some form of investment portfolio, from individual investors to professional asset managers.

Most often, model portfolios are created by using mutual funds. Advantages to using mutual funds are lower entry costs to investing, lowering risk by adding diversification, and access to professional investment management. Disadvantages of mutual funds are expenses and fees, blanket investment advice, and potentially predatory investment managers.

This guide will help you determine how a model portfolio fits into your financial goals, and how to filter through a sea of models. The most common strategy is called asset allocation. We will discuss this and other common strategies below.

Income, Balanced and Growth Asset Allocation Models

Investing strategy is defined by investors goals. The 3 choices available are income, growth, and preservation of capital. You can also choose a balanced strategy that compromises amongst multiple goals. Income is seeking out current income in exchange for capital appreciation potential. This is usually done with bonds and dividend stocks. Growth is seeking capital appreciation in hopes of your investment values rising. This is often done by investing in high volatility stocks like technology and small cap companies. Preservation of capital is seeking to just hold the same worth over time without desiring income or growth. This is often done with cash or short-term bonds.

3 Easy Asset Allocation Portfolios

Before we describe asset allocation models, we want to make sure that you have a clear understanding of what asset allocation is. Asset allocation is one of the most popular methods of investing.

We can loosely define asset allocation as dividing your assets amongst a group of equities. This will be explained below but imagine multiple buckets of investments that all get different amounts of cash based on factors like volatility or the expected future of the economy.

There are multiple options, and we will give you some ideas but it's prudent to discuss the ones you're likely to see.

What is an Asset Allocation?

The most popular model utilizes a strategy called asset allocation. This strategy picks the "weights" for your portfolio based on asset classes. Let's break this down.

Portfolio weights are how much of your overall account or investable dollars, are given to any specific investment. Most investments are called securities. If you have $150,000 of investable dollars, and you put $50,000 each into 3 different investments, we can say each asset has a 33% weight.

The idea of asset class will depend on what you put your money into. If you chose those 3 investments to be an overall stock market mutual fund, bonds, and real estate or commodities, then they would all be different asset classes.

What about Portfolio Rebalancing?

Rebalancing your portfolio is reallocating your asset weightings based on either personal or market circumstances. Using the previous scenario, let's imagine that the stock market has gone on a spectacular bull run, just like the one that we see right now, in March of 2024. The mutual fund, for example SPY, which tracks the S&P 500 index, has risen in value. What was once $50,000 is now worth $100,000. If your other two investments stay at their original value, then that stock market fund is now $100,000 out of $200,000 total. That means that the fund is at a weight of 50% of your account.

Regardless of your model portfolio, something any wise investor will remember is to rebalance their portfolio or change their models.

Should you choose to rebalance, you may have to account for taxes in a taxable brokerage account/ Most often a rebalance is when you sell profits from an inflated fund and reallocate the profit where you see fit. The decision depends on your strategy and the model that you seek to use at that current point in time. We recommend considering different strategies that shift with your own personal life.

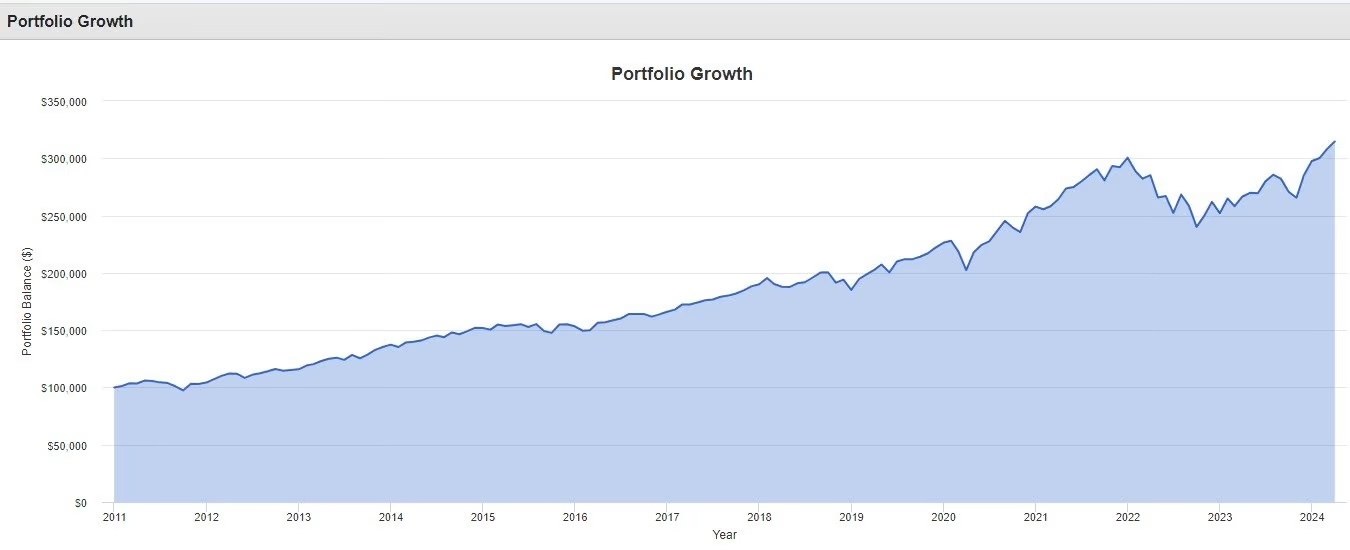

The 60/40 Model Investment Portfolio

The 60/40 name comes from putting 60% of your account into stocks and 40% into bonds. Investors don't need particular expertise or previous investing experience to use this model. The 60/40 portfolio is a model meant to enhance diversification and create a safer portfolio that gives investors a balance of risk and capital preservation or fixed income. The focus here is lower risk and raise risk adjusted returns.

This model is marketed to deliver satisfying gains while minimizing the risk of equity markets with the safety of bonds. Unfortunately, the model doesn't always work as intended. Historical data can show that these model portfolios usually need specific advice for each individual client. Many investors use exchange traded funds (ETFs) to accomplish this, and big companies benefit from ETF models because of the fees associated with those traditional models.

Here we see the growth of a portfolio that’s comprised of two funds for a 60/40 split.

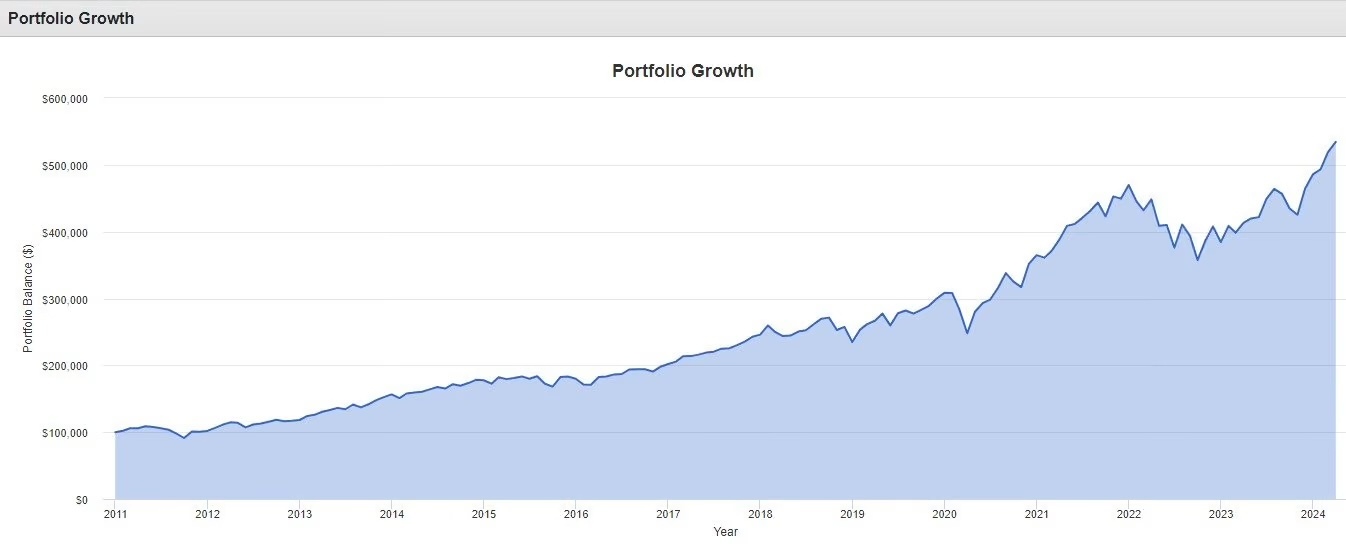

The Three-Fund Portfolio

The three fund portfolio is similar to 60/40 models. They are thought to have slightly more risk with the ability to achieve more returns. Three fund models are another of the most popular investment strategies. Typically you will see an investor choose a whole US stock market fund, a US or global bond fund, and a world stock market fund. The volatility is supposed to be minimized because many funds are supposedly well diversified. One problem that exists with these models is that an investment can occur between multiple funds.

You can achieve decent results from this kind of model, but you again lack truly personalized strategy. Future results can compensate for the generalized advice, if you can afford to endure unfavorable market conditions. Your strategy should never rely on one individual sector or investment. This is one problem with a portfolio like the three-fund model.

Here we see the growth of a portfolio that’s comprised of three funds representing the overall stock market, bond market, and international stock market.

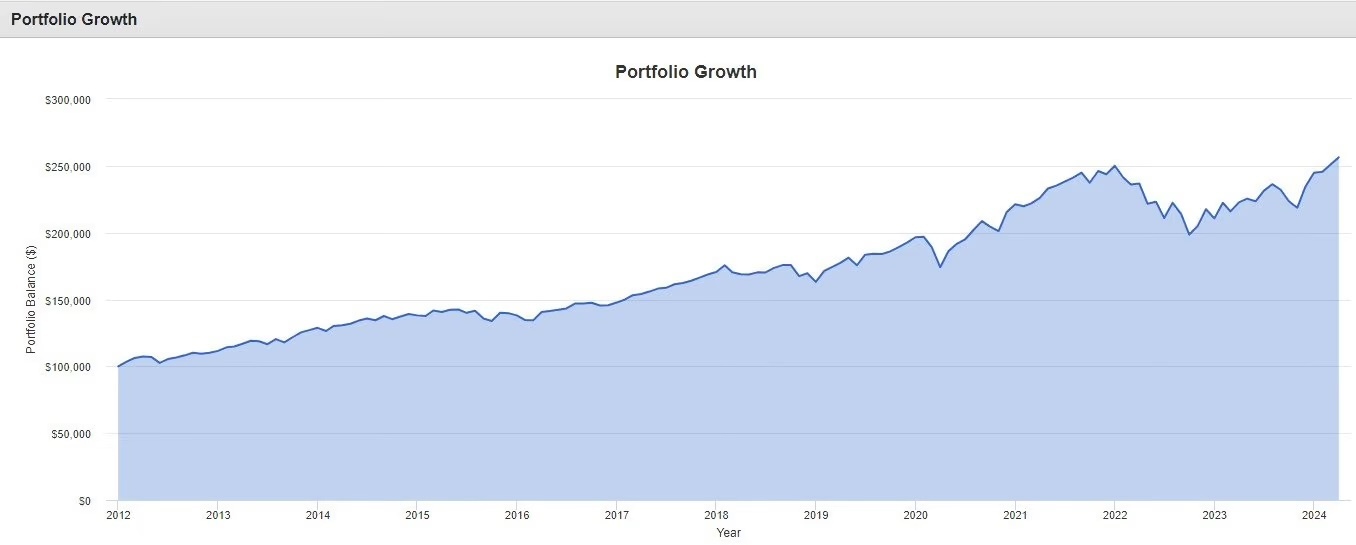

100% Stock Portfolio

This model would have you only use 100% stocks. This can be accomplished with different methods, for example sector rotation between stocks in industries like tech or consumer essentials. Regardless of the tactics, 100% stock models don't use bonds. Typically, this model relates to buy and hold investors who use a strategy such as only one mutual fund that follows the broad "stock market". In more detail, only using one investment like VTI, SPY, or IVV. Each security listed here is a market capitalization weighted fund. These are 100% correlated to market conditions because the most popular stocks with highest growth potential also means bearing the highest risk.

As of late, many investors are also using 100% stock portfolios to substitute for traditional fixed income models, by investing in only dividend producers. This kind of asset allocation model is often frowned upon for not incorporating common elements of risk reduction such as bonds.

Here we see the growth of a portfolio only made of a 100% overall stock market ETF.

The Problem with Asset Allocation Models

In the chart above, the worst dip in the S&P 500 is a 22.34% decline. At this point the retail investor portfolio was down 37.29%. The worst for retail investors is a 39.54% decline. At this point the S&P 500 was down only 17.99%.

Asset allocation as an investment strategy isn't the absolute worst method of investing. It comes with its own set of tradeoffs, as does any investment strategy.

Here is a deep dive on the pros and cons of asset allocation models:

They Simplify Decision Making

The average investor doesn't have significant expertise in the world of investing. We've had many conversations with clients and prospects from all walks of life. Some desire a closer look at the research, understanding, and focus that comes with professionally managed assets. Others decline the investment management learning process because they simply seek a professional to delegate to or self-manage investments with as much ease as possible. This is where model portfolios help the most.

Simplicity is the biggest advantage that asset allocations offer. For investors seeking simplicity, asset allocation is a fine method. As described, you aim for X percentage of value into each chosen asset class. You don't have to stress about nitpicking assets. The only factors to choose between are which asset allocation template you use, and how often to rebalance if at all.

Keep in mind that if you never rebalance your portfolio you will stray from the original allocation, and your model is no longer what you are invested in.

They Aren't Dynamic

While you can adjust your model, asset allocation is often very flat. Many investment advisors will typically use something like a 60% stock to 40% bond portfolio and leave investors in something which is propagated as zero risk. They may also leave rebalancing for each year's end, which ignores clients' life changes. Risk doesn't wait to increase only once per year. It can spike within the market very suddenly.

Investing is much more complex than this. It doesn't make sense to use a tool that is actually shown by data to hurt clients. Why use an investment strategy that doesn't deliver the expected outcome? Historical data shows that traditional asset allocation models often have very poor risk adjusted returns.

They Encourage Laziness

Many individuals will come across a model portfolio with the aim to reduce costs, chase high returns, or other factors of influence. This alone is the main benefit and importance of attempting to create a model. No problem inherently exists with that. A problem is only created when investors who lack confidence or education then use that model to ignore decision making. Specifically, lazy financial advisors who only care about annuitizing income from their clients without putting in genuine effort to give clients an optimal investment strategy. Why leave clients in static portfolios rather than adjust strategy with life changes? Big business often ignores the individual needs of clients and prefer to place clients in an asset allocation model. This is because they raise cash by collecting fees for selling and owning funds. Investment advisors often get a bad reputation for ignoring their clients' needs and using blanket recommendations despite changing market conditions.

How to Find an Advisor you can Trust

There will almost always be a conflict of interest in that financial advisors and planners have a personal benefit of managing your money. With that in mind, you can seek out a fiduciary who is legally obligated to act in your best interests. Here is a free guide to helpful questions you can ask when interviewing a financial advisor. The accuracy of their answers compared to their marketing data will be one gauge to help measure reliability. Another way to filter for trustworthy advisors is to learn about their business mission and their philosophies regarding investment management.

You will always want to find a financial planner or advisor whose values align closely with your own. This rings true with matters like cash flow and also desire to utilize risk in portfolios. Their models should not contain risk far outside of the bounds your financial plan can tolerate.

How much does a model portfolio cost?

A model portfolio can be completely free! Just remember that free does not mean worthless. You may also end up paying more than the value you gain from a poorly devised strategy. All investors' portfolios should be based upon data containing relevant metrics. Don't choose your investment plans off of advertised return alone. Remember that models may only boast their best performing statistics and gloss over other key data. Please consider your own personal financial goals and how they fit into your financial plan before utilizing a model portfolio.

FAQ

What are Model Portfolios?

Model portfolios are a way for investment to be simplified. Models simplify strategy by helping to select each investment for a portfolio. This is wonderful for any investor who doesn't have the time, knowledge or temperament to manage their own investments. Your investment performance can be more or less consequential depending upon your reliance on your investment portfolio. Not all models are made for everyone and while some are marketed as one size fits all, your strategy should always be based on your individual needs whenever possible.

Should I use an Asset Allocation Model?

You should consider using an asset allocation model if you are an investor who lacks the ability to refine your investment portfolio in fine detail. If you need an easy answer to investment selection, asset allocation may benefit you quite nicely. Just be aware of the tradeoffs you face, simplification in exchange for advice that wasn't made for you specifically.

Will my Strategy Work in any Market?

All investors should understand that there is always risk in investing. Everyone has bad picks, and no investment is 100% bear market proof. Well-crafted strategy can minimize risk during adverse market conditions, but you will likely need to change the original strategy to maximize your protection.