How to Navigate the Retirement Risk Zone

The retirement risk zone is the period of time beginning roughly 10 years before retiring and ending roughly 5 years into retirement.

During this transitional period you will shift from a lifetime of accumulating, to beginning to plan how you will draw down and/or preserve the assets you have accumulated.

Our goal with this guide is to help you identify the 9 most common retirement planning mistakes to avoid while navigating the retirement risk zone.

Table of Contents

- Not having an expense tracking system

- Not having a ROTH contribution and/or conversion strategy

- Claiming Social Security benefits "because you can"

- Not consolidating old employer retirement savings (or IRA) accounts

- Not starting your retirement plan early enough

- Having undocumented financial wishes

- Not tracking the right metrics

- Obtaining your financial advice off of the internet

- Not working with a firm like Peak Financial Planning

Retirement Mistake #1: Not Having an Expense Tracking System

The most common retirement mistake is not having a system to track expenses.

No one loves to hear it… But retiring successfully has less to do with retirement savings and more to do with cash flow.

If you overspend in the early years of your retirement, you increase the risk of running out of money while alive.

If you overspend as you approach retirement, you run the risk of not having enough money saved FOR retirement.

This is a retirement mistake you can avoid by having a system to track your spending.

I’m not talking about a budget where you set limits to spending based upon categories, although that may be warranted in some cases.

Rather, I am talking about having a system (or a tool) that allows you to track how much you spend each month broken into two categories - Fixed Expenses and Desired Expenses.

This is CRITICALLY important - the only way you can figure out how much income your portfolio assets will need to generate for you each year is if you know how much you hope to spend each year.

You can use this quick formula to identify how much retirement portfolio income you’ll need each year:

Estimated Spending minus Guaranteed Income (Social Security, Pensions, Annuities) = Required Portfolio Income

The earlier you begin tracking your expenses, the easier it is to project your estimated spending in retirement → The easier it is to plan how much you’ll need in saved moneys in order to retire → The easier it becomes to adjust your savings pattern so that you end up with the right amount of money AT your target retirement date.

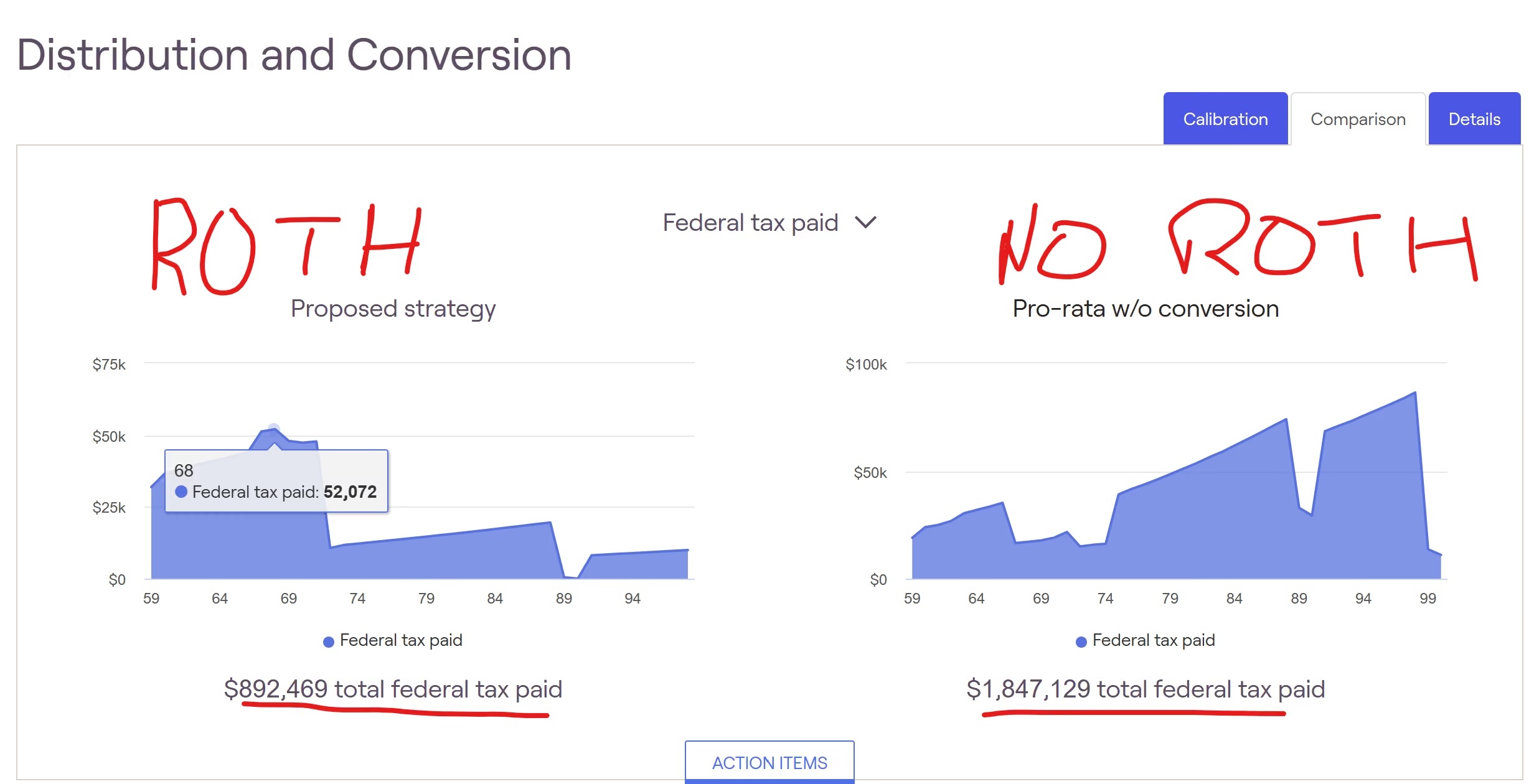

Retirement Mistake #2: Not Having a ROTH Contribution and/or Conversion Strategy

Income Taxes will be your LARGEST single expense in retirement (and over the course of your life!).

All signs point to tax rates increasing over time.

With fewer young people entering the workforce (shrinking tax base), more people relying on government welfare programs (social security and others), and the government continuing to increase its debt levels, the government will be forced to increase tax rates.

ROTH contributions and conversions are one of the best proactive tax planning tools accessible to the general public.

ROTH money allows you to pay taxes NOW and never pay income taxes on those funds (including gains) in the future.

Contributing to a ROTH retirement account allows you to save a certain amount each year in this manner.

If you don’t have significant (or any) ROTH contributions, ROTH CONVERSIONS allow you to convert tax deferred (think 401k or IRA) money into a ROTH format.

Crafting (and executing) a ROTH contribution and conversion strategy as early as possible can have incredible impacts on how much money you can spend during your retirement, as well as preserving wealth that is transferred to heirs.

Not having a ROTH contribution AND conversion strategy in place at least 10 years prior to your retirement age is one of those retirement planning mistakes that is easy to avoid but hard to make up for.

Retirement Mistake #3: Claiming Social Security Benefits “Because You Can”

Whatever your opinion of the long term viability of the Social Security administration, social security is likely to be one of the most valuable sources of retirement funds for retirees with less than $3 million in investable money.

It’s also such a political hot button that it is unlikely that it ever goes away entirely.

Social Security is an annuity (income that you are not responsible for managing the underlying investments!) that is inflation adjusted and guaranteed by the US government for life!

It’s hard to calculate the unique value of that combination of factors.

Whether to claim at 62 (because you can) or to delay and capture the guaranteed increases due to deferral will be one of the most important decisions you make.

This decision is influenced by several factors -

Whether you are forced into retirement early (and unpreparedly)

Whether you have saved assets sufficient to fund you until your optimal social security claiming age

How influential your specific social security income will be to your retirement success

Building a model that factors in your savings rate, your accumulated assets, your desired spending in retirement, and a projection of your social security income at all ages beginning at 62 will help you make the best decision for your unique circumstances.

Don’t just claim social security blindly “because you can”, or because you hit full retirement age.

Claiming Social Security is a permanent decision... Neglecting this evaluation in favor of focusing on retirement portfolio is by far one of the most common mistakes in retirement planning.

Retirement Mistake #4: Not Consolidating Old Employer Retirement Savings (or IRA) Accounts

Having a bunch of small (or large) retirement accounts that are spread between different employer plans or custodians increases the complexity of summarizing your financial picture.

The less clear your financial picture is, the more likely you are to make uninformed or sub optimal decisions.

A couple of examples that I see all the time:

Old retirement accounts are left unattended after separation from an employer. Little does the client know that the investments in that account are in a very conservative target date fund that is yielding subpar returns. That client has lost years of compounding that they can never get back as a result.

Or - a client has 6 retirement accounts spread between various IRA’s and 401ks. Little does the client know that ALL the accounts are invested in an almost identical mutual fund. This makes their portfolio VERY sensitive to market fluctuations because they lack the protection diversification offers.

Consolidating these accounts makes them easier to monitor and therefore manage.

It can also help prevent lost money! You’d be surprised at how many forgotten 401k’s/IRA’s exist simply waiting for their owners to claim them…

This is one of the worst retirement mistakes because it is so EASY to avoid!

Retirement Mistake #5: Not Starting Your Retirement Plan Early Enough

Albert Einstein called the power of “compounding” “the 8th wonder of the world”. The earlier something starts compounding, the bigger and better the result will be in the future!

Well, interest is not the only thing that compounds - smart money decisions ALSO compound.

For example - the earlier you know how much money you will need in order to fund your retirement, the earlier you can start planning to achieve that goal.

Not only that, but once you know how much money you will need in order to fund retirement, now you can backtrack and identify YOUR earliest possible retirement age!

Knowing how early you can retire based on your current spending, saving, and investment strategies gives you power! Armed with that knowledge, you control your destiny rather than leaving it up to the universe (or blind luck)...

Needless to say, the earlier you can answer these questions, the earlier you can adjust behaviors to align with your goals. What age you retire at as well as how much money you can spend each year in retirement are entirely up to you.

Steering your financial ship is like steering the Titanic rather than steering a speedboat. Retirement mistake number 5 is waiting until the final months before retirement to begin your retirement plan.

It’s not impossible to navigate that lack of runway successfully, but it is exponentially harder.

Retirement Mistake #6: Having Undocumented Financial Wishes

Most couples have one “financial driver” and one “financial passenger”. In most cases, division of labor and specialization are great!

When it comes to your finances, there is a hidden price to this division of labor.

If something were to happen to the “financial driver”, the “financial passenger” would have NO IDEA how to execute the “drivers” financial plan!

Even if that couple were to have enough money to make it through the end of life, the “financial passenger” might be financially uneducated and therefore at the mercy of a predatory financial services industry.

Documenting your financial plans and wishes (not just legacy wishes, but also how much you save, why you save that much, why it goes into which accounts and which investments, and so on and so forth) will allow your partner to continue to execute without being taken advantage of.

A documented financial plan acts as non-financial insurance for the “passenger seat” partner.

Of equal importance, undocumented financial plans “drift” over time. Plans that lack firm commitments end up taking people down a long road to “who knows where”.

Documentation leads to commitment which leads to decisive action which leads to optimal results.

Retirement Mistake #7: Not Tracking the Right Metrics

I call the majority of the financial services industry “Big Finance”.

“Big Finance” is predatory. They use the media to scare consumers and brainwash them into focusing on the wrong financial metrics.

It’s like a magician's sleight of hand trick - while “Big Finance” has you focusing on things like the market rate of return, your 401k (or IRA) balances, and your taxable income, they get to charge you fees for investment management because they have you convinced that investment rates of return are the only thing that positively influences your retirement success.

Bull sh**t.

For instance - did you know that for most retirees, taxes will actually be your biggest single expense in retirement? And that second only to budgeting (planning your spending), tax planning will have the largest impact on your actual SPENDABLE wealth in retirement?

Tracking annual spending, after tax portfolio values, after tax distribution amounts (in retirement) and your PLAN REQUIRED RATE OF RETURN will allow you to focus on the metrics that matter most.

And therefore make the wisest financial decisions from a position of knowledge and stability.

Retirement Mistake #8: Obtaining Your Financial Advice Off of the Internet

Despite the fact that you are likely reading this having found ME on the internet, the internet is not a credible source of financial information.

Articles on the internet are NOT designed to solve problems.

What they ARE designed to do is GET CLICKS.

And we know from social media that the most effective way to get clicks is via FEAR.

Making financial decisions from a place of fear (or any decisions for that matter) is never the right choice.

On top of that most advisors (who you might read online) are laughably under credentialed. They do not need a college degree, or anything other than passing 2 exams that require about 60 study hours cumulatively in order to provide “financial advice” to consumers just like you.

It’s important to clear through the clutter and make sure that the source you are reading from IS in fact credible and has direct experience helping people in your situation successfully navigate their financial concerns.

One way to help clear through the clutter is to read guides or content from Financial Advisors that have the CERTIFIED FINANCIAL PLANNER TM (CFP®) designation.

Less than 25% of active Financial Advisors hold the CFP® designation. Obtaining a CFP® designation requires a college degree as well as 6 financial planning related courses, a capstone, and accumulating 4000-6000 hours of professional experience - a process that can take 18 months to 3 years to complete. On top of that, CFP® designation holding financial advisors and financial planners must act as a fiduciary, and therefore in the best interests of their client.

Retirement Mistake #9: Not working with a firm like Peak Financial Planning

All of these common retirement mistakes are easily avoidable, especially if you partner with a Fee Only Fiduciary Financial Advisor who has your best interests at heart.

We’d love for you to consider our Fee Only Fiduciary CFP® Professional team for the following reasons:

- We will help you document your financial wishes and goals.

- We can help you create a reliable retirement income stream that you understand, and that will outlive YOU.

- We can help you pay the government less so that you have more money to spend on the things you care about

- We can help you craft an investment strategy that you UNDERSTAND and lets you sleep well at night knowing you’ll be taken care of.

Schedule a free consultation with us to learn how we can help you build a comprehensive financial plan that works.