Whether you're ending one job and starting another or simply want to consolidate retirement accounts, you will eventually need to figure out what to do with money saved into an employer sponsored retirement plan.

A retirement account rollover refers to an asset transfer of retirement funds or investments from one retirement account to another.

Are you exploring whether to roll over old retirement accounts?

We are Fee Only Fiduciary Financial Advisors that specialize in providing comprehensive retirement guidance.

You can get in touch with us regarding your specific situation via our contact page.

You can also watch our free masterclass on the top strategy retirees can use to increase their retirement income and avoid running out of money.

Retirement Account Rollovers Explained

The objective of a rollover is to transfer retirement investments from one account to another without creating a taxable event.

When done correctly, all types of rollovers will accomplish this goal.

However, when done incorrectly, a rollover can incur a tax liability as well as early withdrawal penalties.

Because most of us will participate in a rollover of some kind at some point in our retirement plan, it's worth taking the time to understand them in greater detail.

As we end our engagement with our current employer we are faced with two choices:

- To leave our retirement savings in our old employers plan and custody, or,

- To transfer our account over to an IRA rollover account

When it makes sense NOT to perform a rollover

Leaving retirement savings in an employer's custody can be beneficial because 401k/403b/457/TSP plan fees are often very low.

In addition, retiree's and pre retirees can make mistakes in the process of completing the transfer.

When a rollover is performed incorrectly, you may be required to pay income taxes on all or part of the transfer amount, depending on what type of account is being rolled over.

If you're under the age of 59 1/2 and the rollover is performed incorrectly, you will also be liable for early withdrawal penalties in the amount of 10% of the balance.

If a mistake is made due to ignorance, the consequences can be dire.

I recommend consulting with a qualified fiduciary fee only financial advisor before attempting to perform a rollover on your own.

Want to learn more about the right way to qualify and choose a financial advisor?

Click here to watch my free masterclass training which explains how to qualify financial advisors AND the strategies top advisors use to help increase clients retirement income by as much as 30%.

When it makes sense TO perform a rollover

Despite the potential pitfalls, in many cases it can be the correct choice to complete a rollover.

Choosing not to roll an old 401k, 403b, 457, or TSP can sometimes lead to it being forgotten and difficult to retrace.

If you left an employer 5 years ago and at the time neglected to roll your retirement account over, you will at some point need to retrace your steps to locate it and choose a course of action for it.

Neglecting to complete a rollover at the time of separation from your employer can also result in you having quite a few retirement accounts.

Having many accounts in different places can make managing your retirement plans complicated.

Each account may have a different asset allocation and need to be adjusted over time.

They may have different fee structures that make it complicated to keep track of what you're paying.

In addition, multiple accounts in different places will likely have different managers who's opinions may conflict - like having too many coaches on a sports team.

Finally, one limiting factor of a 401k, 403b, 457, or TSP is the limited variety of investment choices in those accounts.

Rollover IRA's do not share this restriction which can be an advantage if your retirement plan calls for a wider range of investment options.

If you'd like some advice on how to perform a rollover correctly, you can contact us here.

Direct Rollover

In most cases you will want to perform a direct rollover, also known as a direct transfer.

A direct transfer is when your employer retirement plan sends your money or investments directly to a new financial institution without you ever taking possession of the funds.

This is usually carried out in a couple steps:

- You will have to open an IRA rollover account

- You will likely have to fill out specific paperwork from your employer as well as your new IRA custodian.

The direct rollover is the preferred method because, barring mistakes, you will not have to pay taxes or penalties on the amount that you rollover.

URGENT NOTE: Although you may end up in possession of a check for the balance of your retirement plan - it CANNOT be in your name. If the check is written to you directly, you are now moving to INDIRECT rollover territory and will need to plan accordingly.

Indirect Rollover

An indirect rollover is when, during the transfer of your funds or investments from one retirement plan to another, the funds end up in your CUSTODY.

If a check is written to your personal name OR if funds are transferred from the retirement account into a personal checking or savings account, you are performing an indirect transfer or indirect rollover.

60 Day Rollover Rule

Indirect rollovers can sometimes be called 60 day rollovers due to the severity of the 60 day rollover rule.

During an indirect rollover your old plan administrator will withhold 20% of the account balance for taxes.

The 60 day rollover rule requires that you fund that 20% gap to your ira rollover account within 60 days out of personal funds.

If you cover that gap within 60 days, the 60 day rollover rule is satisfied and when you next file taxes that 20% withheld by your employer will be refunded to you.

If you DON'T cover that gap within 60 days and are younger than 59 1/2, you may be liable for taxes AND for the 10% early withdrawal penalty, adding further pain to the whole experience.

Also under the 60 day rollover rule is the limitation to only perform one 60 day rollover in any 12 month period.

Sep IRA, Simple IRA, Traditional IRA, and Rollover IRA are all limited by the 60 day rollover rule restrictions - so be wary!

You can read more about the 60 day rollover rule here.

Trustee to Trustee Transfer

Trustee to trustee transfers are another form of direct rollover.

In this case the funds transfer directly from one financial institution to another - with no check ever passing through your hands.

In the trustee to trustee transfer taxes do not need to be withheld from the transfer amount and the transfer is not a distribution and is therefore not considered taxable income.

This type of transfer is usually done electronically via wire transfer or ACATs making it simple and effective and reducing the risk that you will have to pay taxes.

What Types of Accounts Are Eligible for Rollovers?

Transfers from one qualified retirement plan to either another qualified plan or an individual retirement account are eligible for rollovers.

Qualified retirement plans are retirement vehicles that receive special tax treatment in order to incentivize us to save for our future.

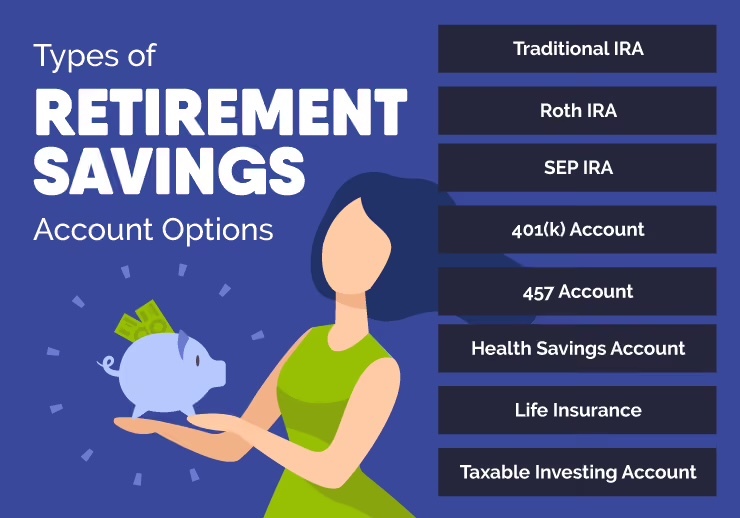

Account types eligible for rollovers include:

- Traditional IRA

- ROTH IRA

- SEP IRA

- Simple IRA

- 401k plans

- 403b Plans

- Thrift Savings Plans (TSP)

- 403b plans

- 457 plans

- Employee Stock Ownership Plans (ESOP)

Rollover FAQ's

Is a Rollover a Contribution?

Rollovers are not considered contributions and therefore will not limit the amount that you will be able to contribute to your new employer sponsored plan, traditional IRA, or ROTH IRA.

Can I Contribute to an IRA Rollover account?

Yes as long as you follow the contribution limits based on the type of IRA rollover account you plan to contribute to.

For traditional IRAs that means $7,000/year ($8,000/year if you are age 50+).

For ROTH IRAs the same contribution limit applies although you will face tighter income limits.

One thing to note is that rollover IRAs are eligible to roll BACK to a 401k type plan - but once you make new contributions to the rollover account you will make it more complex to complete that transfer if you would like to keep that option available.

Does It Cost Money to Do a Rollover?

In some cases there can be a small fee to complete a rollover. This will vary by IRA custodian - you should make sure to ask whether there will be a fee and what that will cost.

How Long Does a Rollover Take?

This can vary by type of rollover. Trustee to trustee transfers will usually be quickest as they are done electronically and remove the friction of having the funds transferred to you before those funds are transferred to their final destination.

In general, expect a rollover to take between 2-6 weeks.

You can ask your custodian for more guidance on this.

Schedule a free consultation with us here