Finding a financial adviser can be difficult but also extremely rewarding.

A recent Vanguard study found that, on average, a hypothetical $500K investment would grow to over $3.4 million under the care of an advisor over 25 years, whereas the expected value from self-management would be $1.69 million, or 50% less. In other words, a financial advisor-managed portfolio would average 8% annualized growth over a 25-year period, compared to 5% from a self-managed portfolio.

And yet, even knowing these numbers, while 71% of Americans say they could use more help with their household financial plan, only 29% of Americans work with a financial advisor or financial planner.

So the question is, why is this the case?

One of the primary reasons why more Americans are not using financial planning services is the difficulty in selecting a financial planner or financial advisor for your specific situation.

Need Help with your retirement planning?

All you need to do is click here to watch a free masterclass training I've recorded.

This free training will discuss the single best change you can make to your financial strategy.

In fact, it's so effective that it may increase retirement income by as much as 30% without needing to invest significantly more time or money.

This is the same strategy that has worked for many of our retirees and pre-retirees.

Once again, click here to watch the free retirement planning training video.

Today I'll be answering the question of “how do you find the right personal financial advisor or financial planner for YOU.”

To begin, I recommend breaking the project down into 7 steps.

- Decide what areas of your financial life you need help with

- Understand the average cost of a financial advisor and how financial advisors are paid

- Understand the difference between small and large financial advisor firms

- Understand the different qualifications and designations that financial advisors can obtain

- Understand the different areas of focus that a financial advisor might specialize in

- Learn how to pick a financial advisor to interview

- Interview several advisors

- Decide what areas of your financial life you need help with

Financial planning can cover a wide range of topics -

- Debt management

- Investment strategy

- Retirement planning

- Investment Management

- Income planning

- Distribution strategy

- Tax planning

- Setting and achieving financial goals

- Budgeting/expense tracking

- Insurance needs

- Emotional and financial transition from things such as death or divorce

- Social security retirement benefits

- And Estate planning objectives

It can be a bit overwhelming to know what YOUR specific needs are from this list.

My advice is to scan the list and understand the terrain of what should be covered during a quality financial planning process.

For example, a certified financial planner may recommend tackling debt management on your own before engaging with a certified financial planner.

As a baseline recommendation, focus on two financial goals to start.

Your first financial goal should be to save and accumulate enough assets that you will not outlive your money

If you are more than 10 years from retirement, your contributions to your retirement assets will matter far more than your investment returns.

This means focusing more on your cash flow and limiting expenses so that you can SAVE as much as possible for your future.

Research shows that once you are within 8-10 years of retirement, investment returns are more influential than contributions.

Substantial market downturns will have a much more material effect on how long your retirement assets will last because you will have less time before reaching retirement age for contributions to make up for the losses suffered.

Financial professionals know this research and can therefore help guide your decision making as you navigate the phases leading up to retirement.

If you want to learn more about the top strategies that can increase income and help you avoid running out of money in retirement, watch this free training video.

Your second financial goal should be to learn how to maintain a predictable standard of living in retirement

Retirement income distribution is a complex process that you want to handle PROACTIVELY.

The decisions you make many years in advance of retirement will determine your ability to make your money last, but also how reliably and consistently you will be able to make withdrawals.

Good financial planners always begin with the above two goals in mind.

The financial planner will design their recommendations and investment management strategy in order to optimize these outcomes.

2.Understanding how advisors are compensated

Financial advisor fee structure will determine the types of recommendations they make to you - the client.

Because of the wide range of financial advisor fees, not all financial advisors will have your best interests at heart.

When you get to steps 6+7, and ask the advisors you're interviewing how they are compensated it's critical that you are able to understand their answers.

That's why I recommend beginning your research by understanding the ways that financial advisors typically charge.

Method #1: Commission Based Financial Advisors

This type of financial advisor gets paid a commission on the front end when you - the investor - select an investment product that they recommend.

They have a relationship with a broker-dealer or insurance company that incentivizes them to share a limited range of products with you.

The financial advisor is compensated for successfully steering you into the broker/insurance company's product.

Relationships with these financial advisors tend to be more transactional.

You tell the advisor how much money you have available to invest, and they present you products or solutions to place that money into.

These relationships usually involve little to no financial planning services.

These types of financial advisors are probably stock brokers, insurance agents, or annuity salespeople.

Of particular note is that the commission based advisor is held to a suitability standard rather than a fiduciary standard.

Suitability requires that investment products such as an annuity or a mutual fund sold for a commission must be suitable for the client but need not be the best possible investment product to meet the client's needs.

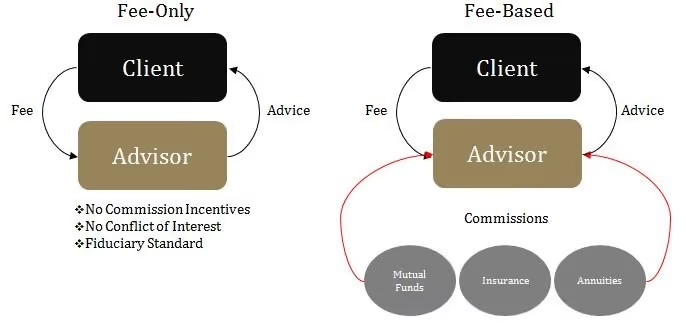

Method #2: Fee-Based Financial Advisors

Fee-Based financial advisors receive a hybrid form of compensation.

The financial advisor might do a “dollars-for-hours” style agreement for a financial plan (think retainer fee or hourly rate - similar to a CPA or lawyer).

In addition, the financial advisor may also receive commissions for successfully steering you into investment products of companies with whom the financial advisor is affiliated.

The fee based advisor may position themselves as an investment advisor - saying they only focus on investment management in order to specialize.

They may steer you away from financial planning as it is often not in their scope of expertise.

While the relationship will be less transactional and more familiar than the commission only relationship, most fee based financial advisors do not engage in ongoing financial advice or financial planning relationships with their clients.

In our opinion this leads to less than optimal recommendations because the financial professional has only limited knowledge of your situation and will therefore have gaps in their knowledge.

And, just like commission based advisors, fee based advisors are held to a suitability standard meaning they may not always be working in your best interest.

Method #3: Fee-ONLY Financial Advisors

Fee-Only financial advisors are only compensated by you -the client - and never receive any form of commission or outside compensation.

The fee only financial advisor can be paid a flat fee, hourly fee, percentage of assets under management, or even on a subscription basis.

Most importantly, Fee only financial advisors are held to a fiduciary standard rather than a suitability standard.

This means that their financial guidance must be in the best interest of the client.

Many fee only advisors are also Certified Financial Planners because the regulating body for the certified financial planner requires that they be held to a fiduciary standard.

You can verify that an advisor in question is indeed a fiduciary or fee only by referencing the financial planning association that they may be a part of.

Method #4: Assets Under Management

AUM fees (or, assets under management fees) are universal across all three types of financial advisors.

If you as an investor, choose to delegate the management of your investment portfolio to your investment advisers - the financial advisor will be compensated via AUM fees for their investment advisory services.

The industry average for AUM fees are around 1% of the total value of the assets being managed.

Click here to visit our pricing and services page and learn more about how we work with clients.3. Understand the differences between large and small firms

Because of the wide range of compensation models, not all financial advisors will have your best interests at heart.

When you get to steps 6+7, and ask the advisors you're interviewing how they are compensated it's critical that you are able to understand their answers.

That's why I recommend beginning your research by understanding the ways that financial advisors MAY get paid.

3. Understand the differences between large and small firms

Large National Financial Advisor Firms

Large national firms such as Ameriprise or Northwestern mutual, or even a financial institution like JP Morgan Chase all have something in common.

They are HUGE!

That means resources, broad ranges of experience, research teams, etc.

These are all benefits of the economies of scale that these larger firms have.

They allow specialization and delegation and can be an asset.

There are, however, several downsides to larger firms.

Larger firms typically have incentive structures based around commissions and the sale of firm specific proprietary products.

This means that the financial advisor is incentivized to present a more limited range of products or options to you as the investor.

Financial advisors at these broker dealers typically work on a fee based compensation structure.

They will be titled "Registered Representatives" rather than "Investment Advisor Representatives".

The financial advisors at larger firms are also incentivized to go out and gather more clients rather than focus on the ones they have because they need to sell products to make their money - and new buyers means new sales.

Smaller, Local Financial Advisor Firms

Smaller, local Financial Advisor firms - typically Registered Investment Advisors - are unaffiliated with one specific vendor.

Registered Investment Advisors typically have relationships with multiple custodians and multiple vendors.

Especially if the firm is a Fee-Only or Fiduciary, smaller firms eliminate the conflict of interest that exists in the financial services industry by eliminating compensation structures built around commissions and product sales.

A Registered Investment Advisor may not have the same resources in terms of research departments or large advisory teams.

They make up for that by having a more holistic approach to advising that includes getting to know the client at a deeper level, and creating some form of a longer, more intimate relationship.

Where larger firms may also have asset minimums in order to work with a client, oftentimes smaller firms will not have that same restriction - making them more available to help a broader range of needs.

And finally - working with a smaller firm you will not feel like just another number. You'll have direct access to your advisor and the financial advisor services that comes with that unencumbered relationship.

4. Understand Financial Advisor's Credentials

In order to give investment advice, financial advisors are required to obtain specific credentials.

As with any credentialed industry like the accounting or legal fields, not all credentials are created equal!

The baseline standard in order to be qualified as a financial advisor are the Series 7 and Series 63/65/66 licenses.

These are rudimentary and extremely basic. They provide book learning towards a test which, having completed those exams personally, is completely inadequate to qualify someone to be a comprehensive financial advisor.

Many financial advisors stop there because there is no industry requirement that financial advisors pursue higher learning or credentialing.

As a result, much like the real estate industry, because the barrier to entry to obtain those licenses is so low, each year many new financial advisors join the industry simply to wash out because they lacked the skill or experience to successfully handle complex client situations.

There are a ton of higher education credentialing options in the financial advice space above and beyond the 7 and 63/65/66.

The gold standards of the industry are the

- CFP (Certified Financial Planner) which is regulated by the certified financial planner board

- CHFC (Chartered Financial Consultant) which is regulated by the American College of financial services

- CRPC Financial Advisor (Chartered Retirement Planning Counselor) which is regulated by the College for financial planning.

In addition to these three, there are many other great credentialing programs that indicate the financial advisor in question takes their continuing education and growth seriously.

Which will translate to higher quality service and advice for you, the client.

It's a great idea during the interview process to ask about the financial advisors credentials/advanced education.

5. Understand Financial Advisors Areas of Focus or Specialty

Financial Advisor is a vague, general description of a profession that covers a wide range of professionals.

It could cover

- insurance professionals,

- investment managers,

- financial planners,

- financial coaches,

- or stock brokers.

To make matters more complex, within this soup of professionals, some are considered fiduciaries and have a fiduciary duty and some are not.

So then the question arises - what does fiduciary duty entail?

Fiduciary duty refers to the fact that the financial advisor in question will pledge to put the interest of their clients first.

Any recommendation the financial advisor makes must be made solely with the best interest of the client in mind.

The combination of a fee-only compensation structure with the requirement to act as a fiduciary limit the conflict of interest that may present itself in the financial advising industry.

A good financial advisor should be compensated for the quality of their advice and expertise - not for presenting one corporation's financial product over another's.

As such, regardless of the financial advisors area of focus - if they are both a fiduciary financial advisor and a fee-only advisor, you'll likely receive the most unbiased advice.

6. Research advisors or ask for referrals

As you can see, financial advisors come in many forms with a wide range of qualifications and specialties.

Choosing the right financial advisor requires that you thoroughly research potential financial advisors.

The best way to begin is to ask friends and family.

If they have an advisor they are happy with, it's likely they will be a good candidate to consider.

And now, armed with the information provided here, you should be able to ask the right questions to understand whether that referral will be a good option for you.

Another option is to look for advisors online.

I am personally part of four wonderful financial planning associations that provide free databases of qualified advisors

CFP® (CERTIFIED FINANCIAL PLANNER™)

NAPFA (National Association of Personal Financial Advisors)

Just bear in mind that simply because an advisor is listed in one of these databases does not necessarily mean that they are a fiduciary, nor does it indicate which compensation model they work under.

7. Interview Several Advisors & Come Prepared With Questions

Once you arrange meetings/interviews with financial advisors, here is a list of questions you can come prepared with.

Again, armed with the information provided here, you should be able to understand their answers in a way that allows you to make a wise decision.

- Are you a fiduciary?

- Are you always acting as a fiduciary? (Some fee-based advisors may not always act as fiduciaries when selling commission-based products.)

- How are you compensated?

- What is your approach to financial planning?

- What financial planning services do you offer?

- What kind of clients do you normally work with?

- Do you have any account minimums?

- Do you have any conflicts of interest in managing my money?

- What information do I need to bring for you to look at when developing my financial plan?

- How many times and how often will we meet?

- Will you collaborate with my other advisors, like CPAs or attorneys?

In Summary

Identifying the right Financial Advisor for you may feel overwhelming. While you should remain cautious in your decision, the right financial advisor for you can truly unlock your financial potential and help you achieve your goals.

Find a local independent financial advisor. Visit our Contact Us page to get in touch with us.