A 457 b is a tax advantaged retirement savings plan available to some state and local government employees as well as some non-profit organizations.

While similar in many ways to the more common 401 k retirement plan, 457 b plans are non qualified savings vehicles.

On top of being a nonqualified plan, 457 b plans have some important differences that could be considered advantages when used properly.

Let's dive into what you need to know about 457b retirement plans.

Do you need help building and managing your retirement plan?

You can begin by watching our free masterclass on the top strategy retirees and pre-retirees are using to increase their retirement income and avoid running out of money.

What are 457 b plans?

457 b plans are tax deferred, employer sponsored retirement savings accounts available mostly to civil servants, local government employees, law enforcement and public safety employees.

Specifically, police officers, firefighters, public school teachers, government officers, paramedics, and municipal employees.

Contributions to 457 b plans are taken directly out of employees paychecks and automatically saved to the 457 b retirement account.

These contributions can be taxed in one of two ways.

Traditional 457 b

Traditional 457 b contributions are made pre tax meaning they are deducted from your paycheck before taxes and lower your current year’s tax bill.

These contributions grow tax free until retirement. You do not pay any capital gains taxes when you buy or sell investments in traditional 457 b accounts.

An added bonus of pre tax 457b contributions is that they lower your taxable income - when you pay taxes at the end of the year you pay taxes on fewer dollars!

Roth 457 b

Roth 457 b contributions are made post tax, meaning they are deducted from your paycheck AFTER taxes have been paid on that amount.

Paying taxes on the contributions in the current year allows for tax free withdrawals when you retire.

And, just like the traditional 457 b contributions, you do not pay any capital gains taxes when buying or selling investments in the Roth 457 account.

What are 457 b plan contribution limits?

Similar to other employer sponsored retirement plans, 457 b plans do indeed have contribution limits that must be followed.

For 2024, the maximum allowable contribution to a 457 b plan is $23,000 which includes both employer and employee contributions.

457 b plans have catch up contribution rules

If you are age 50 and older, you may contribute the "catch up" contribution amount of $7,500 making for a total allowable contribution limit of $30,500 in 2023.

457 b plans ALSO have two unique contribution features that allow you to potentially save significantly more than other employer sponsored retirement plans.

The first of these unique features is that three years prior to your retirement you can contribute up to double the eligible contribution amount or 100% of your salary, whichever is less.

There are two restrictions that must be followed to make use of this unique feature.

- The bonus contributions cannot exceed the amount of unused eligible contributions from previous years. To clarify - let's say you had contributed $17,000 per year for the 5 prior years out of a possible $23,000 per year. You would have accumulated $6,000 x 5 years ($30,000) of "unused eligible contributions" that could then be used during this 3 year catch up period. If, conversely, you had contributed the maximum allowable each year, you would not be able to use the bonus "3 year pre-retirement" contributions.

- The second restriction is that the $7,500 of age 50+ catch up contributions cannot be used if you are also utilizing the "3 year pre retirement" bonus contributions.

This means that if you're within three years of retirement you could contribute UP TO $45,000 but cannot use the age 50+ catch up contribution allowance if opting for the three year rule.

The second unique feature available to 457 b plans is that, because it is not considered a QUALIFIED retirement plan, if you have access to another employer sponsored retirement plan you would also be able to contribute up to the employee maximum to both plans!

In 2023, that would equate to being able to contribute $23,000 to both a 457 b plan AND a 403 b plan! If you are age 50 and older, you can use the $7,500 catch up contribution allowance, but only for one plan - not both.

So in this case the maximum you would be able to contribute in 2023 would be $53,000.

What are 457 b plan withdrawal rules?

The advantages 457 b plans have over 401 k and 403 b plans continues when it comes to your ability to withdraw funds from your account.

There are no early withdrawal penalties when withdrawing funds from 457 b plan accounts.

So as long as you have separated from your employer, if you are under normal retirement age of 59 1/2, you can tap into the money in your 457 plan without paying the 10% early withdrawal penalty.

NOTE: that if your 457 b is a traditional account, you will still need to pay income taxes on the that money.

Is there a 457 b Roth option?

Yes - ROTH 457 b plans exist.

But your employer must make that option available to you.

Not all employers offer a ROTH option within their 457 plan.

What are the 457 b required minimum distribution (RMD) rules?

457 b accounts are bound by the required minimum distribution (RMD) rules similar to other traditional retirement savings accounts.

This means that once you reach age 72 you will be required to take minimum distributions from your 457 b account.

The amount of the RMD is determined by an IRS table that is based on prior years ending account balance as well as your age and life expectancy.

When the RMD funds are distributed, you will be required to pay income tax on the money withdrawn if it comes from a traditional account. ROTH 457 b accounts are not subject to income taxes on RMDs.

NOTE: Some 457b plans will have options for hardship distributions or in-service distributions. Please check your plan document or ask your plan administrator for the particular rules surrounding these withdrawal options.

How do 457 b plans compare to other retirement savings vehicles?

Clearly there are some advantages 457 b plans have over comparable employer sponsored retirement accounts.

The 3 year contribution allowance, being able to contribute to multiple employer sponsored retirement plans simultaneously, or being exempt from early withdrawal penalties are all unique to the 457 b plan.

457 vs 403b

As previously stated - 403 b plans are required to adhere to the 10% early withdrawal penalties if you withdraw money before age 59 1/2 (with some rare hardship exemptions).

Not so for the 457 plan.

But - similar to the 403 b plan, 457 b plans are indeed subject to RMD requirements.

One advantage the 403 b may have over the 457 b is that employer contributions to a 403 b do not count towards the total eligible employee contributions limits. This can result in the 403 b having a higher total allowable contribution limit.

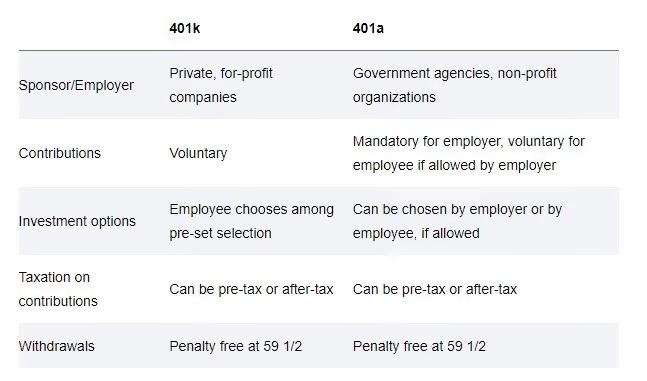

401k vs 457 and 401a vs 457

Just like with 403 b plans, 401 k plans are subject to a 10% early withdrawal penalty if you are under age 59 1/2 - even if you have separated from your employer.

Again, similar to 403 b plans, 401 k plans are also subject to RMD requirements.

The 457 b is not subject to either.

But the 401 k plan does have one advantage over 457 plans - 401 k plans will frequently offer an employer match which does not occur in the 457 b plan.

An employer match is essentially free money to the employee as long as you stay with your employer until that money vests.

401a plans function essentially the same as 401 k plans and will therefore have the same advantages and disadvantages.

You can read more about 401a and 401 k plans here.

457 b plan rollovers

Government 457 plans can be rolled over into any other retirement account so long as you have left your employer.

This includes 457 rollover to IRA, to a ROTH IRA, SEP IRA, or another government 457 b plan. You can view the Internal Revenue Service chart that shows rollover eligible retirement accounts here.

However, if your 457 b plan is via a private tax-exempt employer, you will have limited rollover options. You will only be able to roll your 457 b funds into another private 457 b plan.

In this case if you are retiring and will not have another eligible 457 b plan to roll the funds into, the entire balance will be distributed to you as a lump sum and could potentially push you into a very high tax bracket - leading to a giant tax bill...

If you need help crafting the best strategy for your 457 b or other retirement assets, consider working with a fee only financial advisor.

Summary

Regardless where you are employed, you should be considering using tax deferred retirement savings options. If you are a government employee and have the option to choose between a 457 b and a 403 b, hopefully this guide will help you consider your options and make the best choice for you.

It's also important to note that regardless what employer option you have, you can still open a ROTH or Traditional IRA on your own and should consider how this can supplement your existing retirement plan options.

Find a local independent fee only financial advisor. Visit our Contact Us page to get in touch with us.